Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments Jun 1, 2026

Jun 1, 2026

Key Takeaways

- Choose a short-term payment plan when the balance can be cleared within 180 days; use a long-term installment agreement otherwise

- Apply through the IRS Online Payment Agreement tool when all required returns are filed and compliance is current

- Set a monthly payment based on your worst cash-flow month — default reopens collection action including federal tax lien risk

- Consider Currently Not Collectible status or an Offer in Compromise before committing to payments you cannot sustain long-term

- PriorTax files back taxes accurately and affordably so every payment plan starts with correct numbers from the start

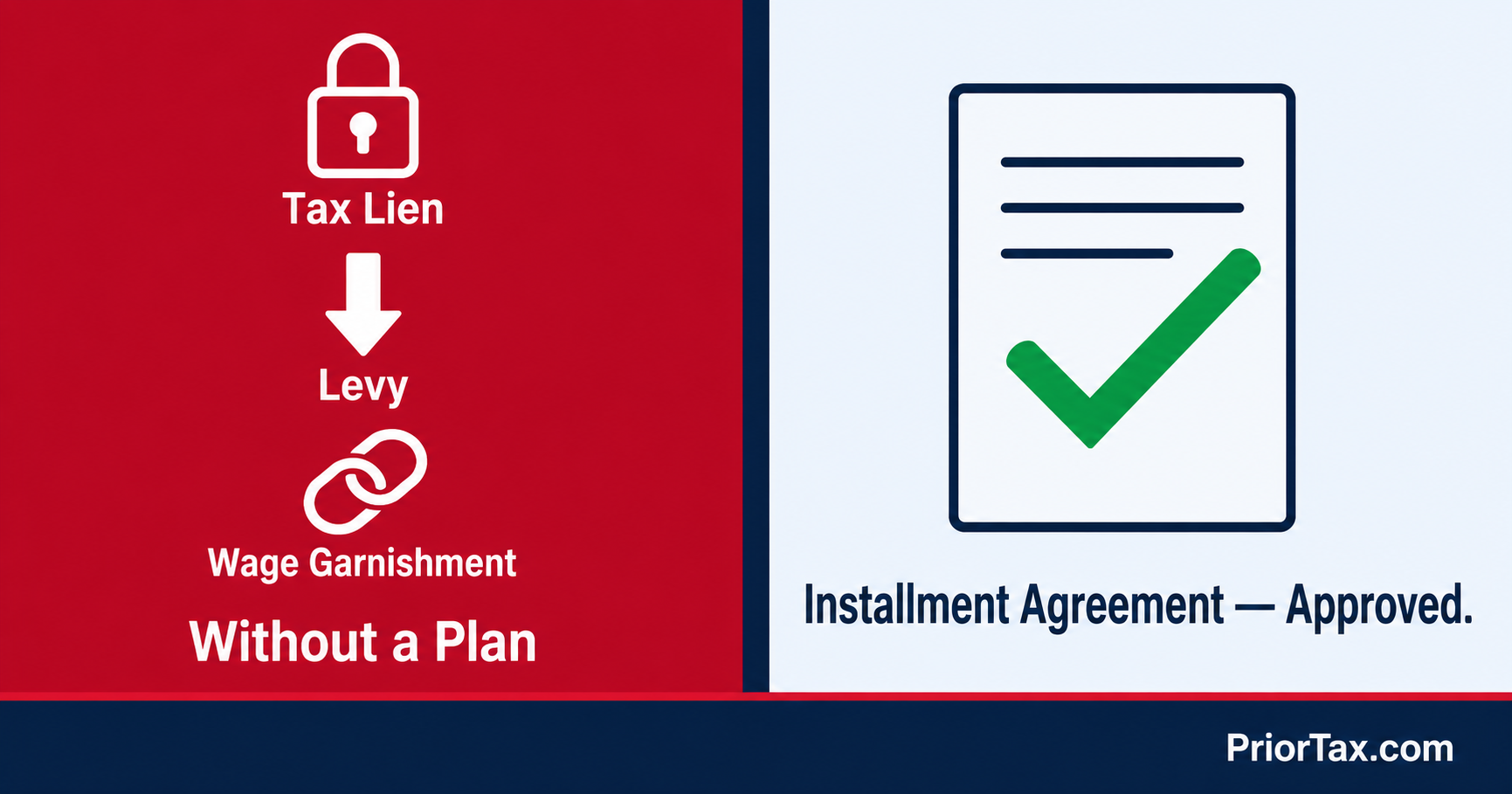

A tax bill you cannot pay in one shot is a cash-flow problem, not a reason to stop engaging with the Internal Revenue Service.

For many taxpayers that need assistance, an IRS tax payment plan creates a structured path to resolve prior taxes while reducing the chance that the account moves toward enforced collection.

This PriorTax guide explains how installment agreements work, who qualifies, what they cost, and how to choose terms you can keep.

What an IRS Payment Plan Is (And When It Helps)

An IRS payment plan, usually called an installment agreement, is a formal arrangement that lets you pay a tax debt over time instead of in a lump sum.

The key point is practical: the plan buys time and structure, but it does not freeze the account because interest and the failure-to-pay penalty generally continue until the balance is paid in full.

At PriorTax, we emphasize that filing the return on time still matters even if payment is impossible, because the failure-to-file penalty is usually steeper than the payment penalty.

That distinction changes the math for anyone behind on taxes, which is why taxpayers dealing with filing taxes late should treat filing and paying as two separate decisions.

Approval is not automatic, since the IRS looks at your balance, filing compliance, and whether the proposed payment is credible.

A current agreement can help prevent escalation toward a levy or other collection pressure, but only if you keep making payments and stay current on future taxes.

Payment Plan vs. Paying in Full

Paying in full is always cheaper because it stops future interest and shortens the period that penalties can accrue.

A payment plan is the better tool when full payment would force you to miss rent, payroll, or other essential obligations.

Common Reasons People Need a Plan

Most payment plans start with a withholding shortfall, self-employment underpayment, or an unexpected tax bill after credits or deductions change.

Others arise after job loss, medical costs, or a period of assistance with back taxes when multiple filings are being brought current.

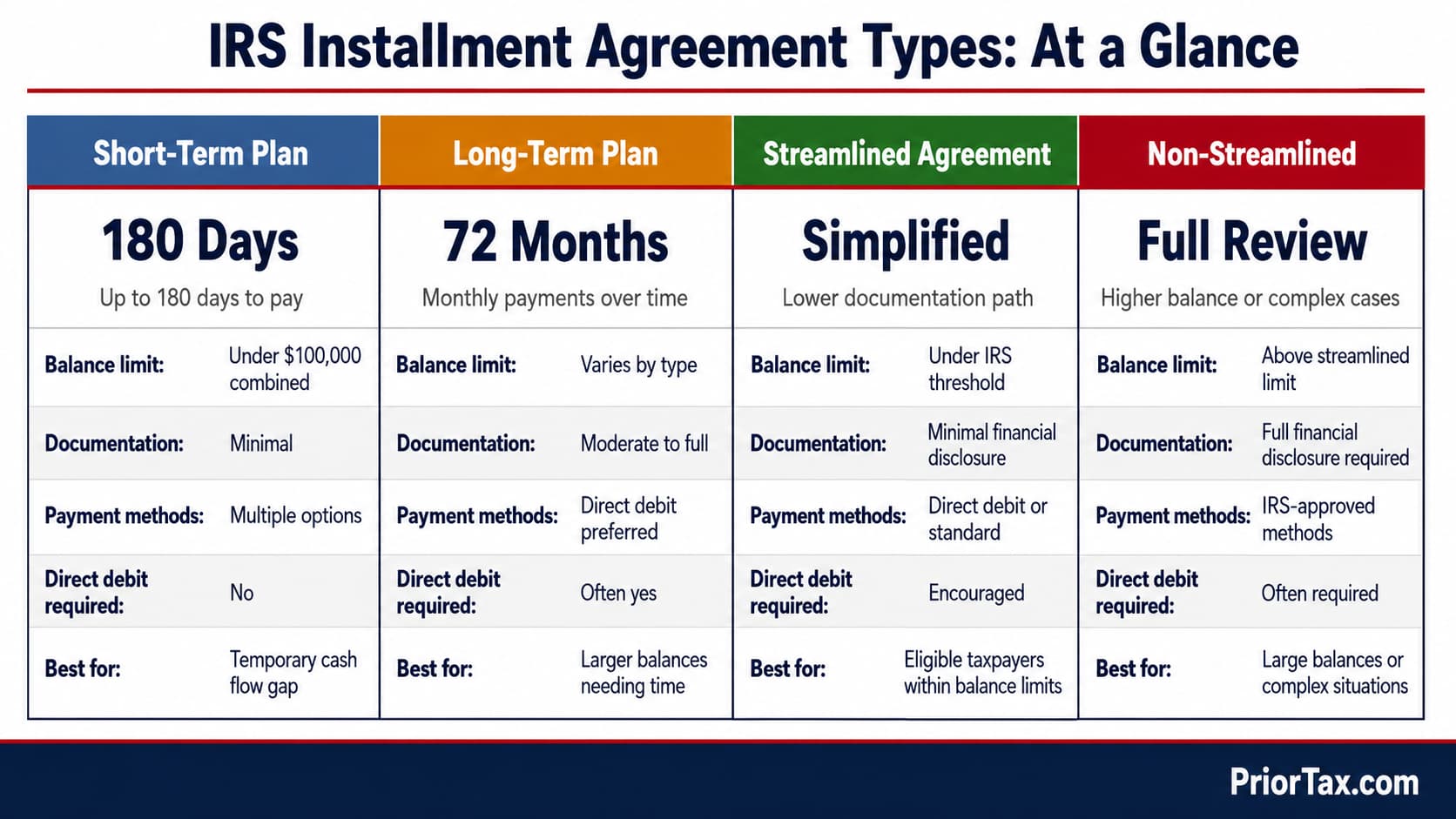

Types of IRS Installment Agreements

The IRS generally offers short-term plans for balances you can clear within 180 days and long-term arrangements for debts that need more time.

That split matters because a short payoff period usually means fewer administrative steps, while a long-term payment plan often requires more attention to payment method and risk of default.

You will also hear the term streamlined installment agreement, which usually refers to a simpler approval path for eligible taxpayers within certain balance thresholds. By contrast, non-streamlined requests may require fuller financial disclosure, and the exact terms available can change based on how much you owe and whether all required returns and payments are current.

Direct debit is encouraged because it lowers missed-payment risk, which is one of the main reasons agreements fail.

Taxpayers handling prior-year tax filing issues should assume the IRS prefers automation over promises, since automatic payments create a cleaner compliance record.

Short-Term Payment Plan (Up to 180 Days)

A short-term plan works best when the problem is temporary, such as a bonus arriving next quarter or a receivable clearing soon. If you can realistically pay within 180 days, this option usually involves less friction than a longer agreement.

Long-Term Installment Agreement (Monthly Payments)

A long-term installment agreement spreads the balance into monthly payments, and many eligible taxpayers see terms extending up to 72 months. Payment methods can include direct debit, payroll deduction, or manual payments, but the most stable option is usually the one that removes memory and timing from the process.

Eligibility: What the IRS Looks At

Eligibility starts with filing compliance, because the IRS usually wants required returns filed, or at least actively being filed, before approving an agreement.

Your tax balance due, prior payment history, and current compliance determine which options appear through the IRS payments portal and which requests require more documentation.

The IRS also tests whether your proposed payment amount fits your financial reality.

That review is not only about what you can pay this month, but whether the amount is sustainable enough to avoid default six months from now.

If the payment is not affordable, an installment agreement may not be the right solution. In those cases, alternatives such as “currently not collectible” status or an offer in compromise can be more appropriate than forcing an agreement that fails.

Documents and Info to Gather Before Applying

Gather recent notices, your current balance information, filing status details, and any CP letters before you apply. Banking information for direct debit and a realistic monthly budget are equally important because the strongest application matches the paperwork to a payment you can sustain.

If You Haven’t Filed Yet

File as soon as possible even if you cannot pay, because late filing usually increases penalties faster than late payment.

An extension to file through Form 4868 gives more time to submit the return, but it does not extend the deadline to pay the tax owed.

How to Apply for an IRS Payment Plan (Step by Step)

The fastest route is usually the IRS online payment agreement tool, which lets many taxpayers request terms without mailing forms.

Speed matters because a faster application can reduce the time your account sits unresolved, and unresolved accounts are more likely to generate additional notices.

Choose the plan type and monthly amount based on what you can pay every month, not on what sounds cooperative in the moment.

A lower payment you can maintain is stronger than an aggressive promise that collapses after two drafts.

Direct debit is often the cleanest payment method because it reduces missed due dates and creates a record the IRS can track easily. Once approved, save the confirmation, payment schedule, and any terms tied to keeping the agreement active.

Applying Online With IRS Online Payment Agreement

Sign in to your IRS Online Account to review balances, verify identity, and request terms.

(*** Our team at PriorTax recommends to save screenshots or confirmations because clear records help if a payment posts late or the account status needs correction).

Applying by Mail or Phone (When Needed)

Form 9465 can be used for some requests when online access is unavailable or the account does not fit standard criteria.

Phone contact can help when you have a pending notice, unusual financial facts, or need to modify an existing agreement.

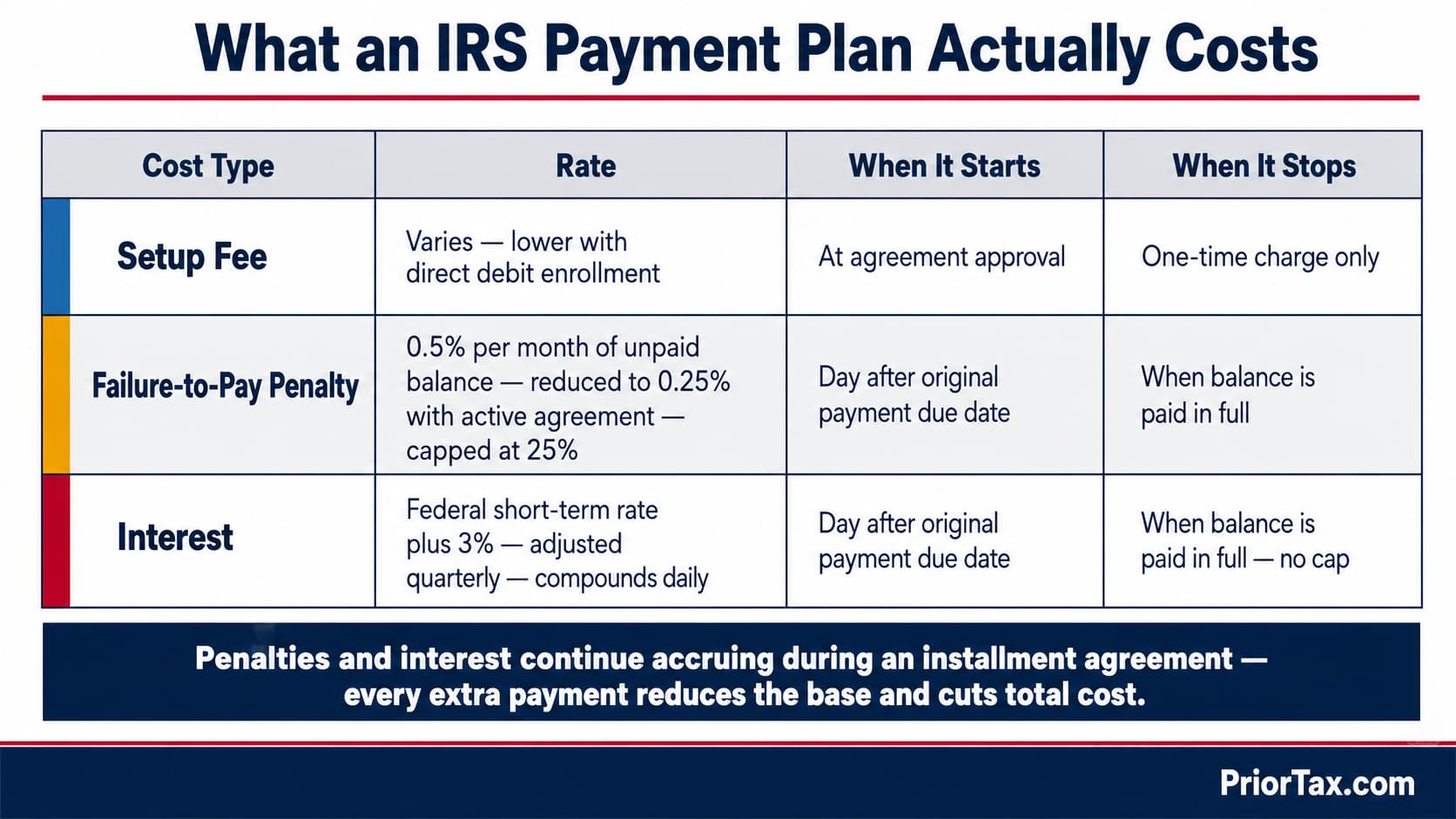

Costs, Interest, and Fees: What You’ll Pay

Most installment agreements involve a setup fee, often called a user fee, and the amount can vary based on how you apply and how you pay.

Direct debit often carries a lower setup fee because it reduces servicing risk, which shows how the IRS prices convenience around the likelihood of default.

Interest continues on the unpaid tax balance until the debt is fully paid, and penalties may continue while the agreement is active. That means the plan solves enforcement risk more than cost, so paying extra whenever possible usually saves money.

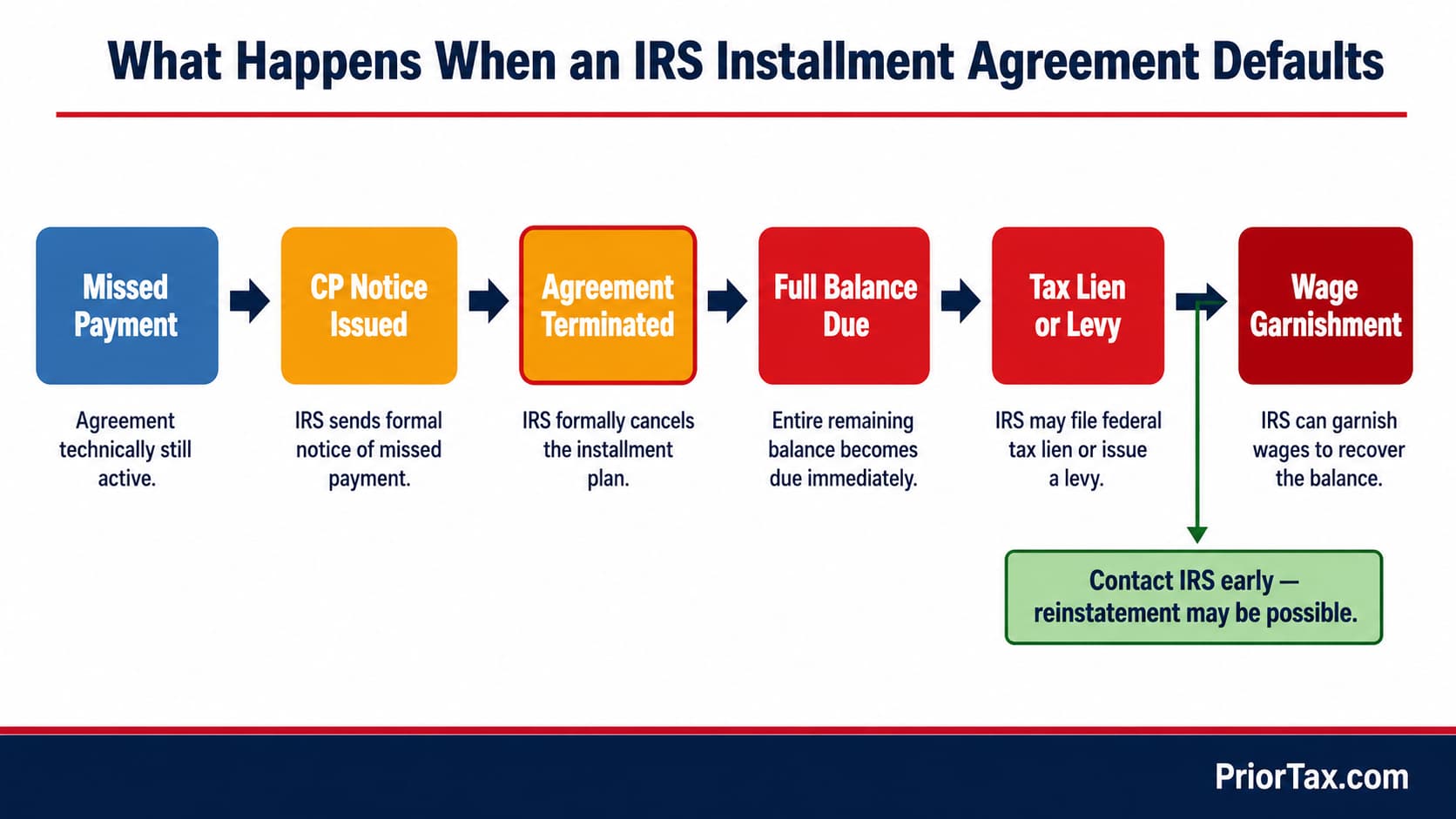

Missing payments can default the agreement and reopen the door to collection pressure.

At PriorTax, we see this pattern often in late tax filing cases where taxpayers focus on the old balance but forget to budget for current-year withholding or estimated taxes.

How Interest Is Calculated (In Plain English)

Interest is charged on the unpaid balance, and the interest rate can change quarterly.

The practical takeaway is direct: every early or extra payment reduces the base on which future interest is charged.

Failure-to-Pay vs. Failure-to-File Penalties

The failure-to-file penalty is typically larger than the failure-to-pay penalty, which is why filing promptly matters even without funds to pay.

A payment plan manages the debt over time, but it does not erase penalties already assessed.

Choosing a Monthly Payment Amount That Won’t Backfire

The right payment amount is the one you can make in a bad month, not only in a good month.

Taxpayers who default often choose a number based on urgency rather than budget, and the IRS would rather receive a sustainable payment than spend time reinstating a failed agreement.

Start with take-home pay, subtract housing, food, utilities, insurance, transportation, and minimum debt payments, then leave a buffer for irregular costs. Self-employed taxpayers need an extra layer here because future estimated payments must fit alongside the installment agreement or a new balance can break compliance.

Adjusting withholding or estimated tax payments is often as important as setting the installment amount.

An agreement that pays old debt while new debt accumulates is not progress, it is account churn.

Quick Budget Method for Setting a Payment

Use one month of actual bank activity, not guesses, to estimate essentials and cash left over. Recheck after 30 days, because increasing a stable payment later is safer than defaulting early on an amount that looked possible on paper.

What Happens After You’re Approved

Once approved, payments are posted to your tax account and can usually be tracked through your online IRS account.

Monitoring matters because catching a failed draft or posting delay early can prevent the agreement from sliding toward default.

Staying compliant means more than making the monthly payment.

You must file future returns on time and pay new taxes as they come due, or the IRS can treat the agreement as broken and resume collection action.

If a plan defaults, the IRS can move toward stronger tools, including a federal tax lien in some cases or other collection action depending on the account history.

By contrast, a current agreement reduces the chance of those steps because it shows active resolution rather than avoidance.

How to Avoid Default

Direct debit or payroll deduction lowers the odds of a missed payment.

If a payment will fail, contact the IRS before the due date because early communication gives you a better chance to adjust terms before the account deteriorates.

How to Modify or End a Plan

You can often request a change if income drops or expenses rise. Paying the balance in full ends the agreement and stops future interest from accruing on the remaining unpaid tax.

Examples and Common Mistakes to Avoid

Suppose you owe $6,000 and enter a 24-month agreement at $250 per month.

If you add occasional extra payments, the balance falls faster, which cuts interest and shortens the life of the plan more effectively than waiting for the scheduled end date.

The most expensive mistake is not filing because you cannot pay, since that can trigger larger penalties and even a substitute return that omits deductions.

Taxpayers who need to file back taxes should remember the 3-year refund deadline, because delay can turn a possible refund year into a lost claim year.

A second mistake is choosing a payment you cannot sustain, followed closely by ignoring an IRS notice after approval.

At PriorTax, our expert review perspective on catch-up filings shows the same pattern repeatedly: old debt becomes manageable only when the taxpayer stops creating new debt and responds to notices quickly.

Mini Case Study: Catching Up After Missing the Deadline

A taxpayer misses the filing deadline, files immediately, confirms the balance, and then sets an installment agreement based on actual cash flow rather than anxiety.

That sequence limits penalty growth, creates documentation, and turns a vague problem into a schedule with dates and proof.

When a Payment Plan May Not Be the Best Fit

If you cannot cover basic living expenses, “Currently Not Collectible status” may be more realistic than forcing payments you will miss. If your financial profile supports a reduced settlement, an Offer in Compromise may deserve review before committing to a long payment horizon.

FAQs

Can you have a payment plan for IRS taxes?

Yes. The IRS offers short-term payment plans and long-term installment agreements for eligible taxpayers who need time to pay a balance.

How much will the IRS accept for payment plans?

It depends on your balance, compliance status, and ability to pay. The IRS usually expects an amount that resolves the debt within the allowed timeframe without causing immediate default.

How long does the IRS give you to pay owed taxes?

Short-term plans are generally available for up to 180 days. Long-term installment agreements can run longer, and many eligible taxpayers see terms up to 72 months.

How much interest will I pay on an IRS payment plan?

Interest accrues on the unpaid balance until the tax is fully paid, and the rate can change quarterly. Extra payments reduce the balance sooner, which lowers total interest cost.

A payment plan works best when it is paired with timely filing, realistic budgeting, and current-year compliance.

If you are catching up on older returns, our professionals at PriorTax bring expert review to the filing side of that process so the payment plan rests on accurate numbers from the start.

Categories:

Leave a Reply

Your email address will not be published. Required fields are marked*

You must be logged in to post a comment.