Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments Jun 9, 2026

Jun 9, 2026

Key Takeaways

- File Form 843 by July 10, 2026 to claim a COVID penalty refund or abatement.

- Refunds apply to penalties already paid; abatements apply to penalties assessed but unpaid.

- Write “Protective Refund Claim Pursuant to Kwong Case” across the top of Form 843.

- Form 843 cannot be e-filed; mail it certified with return receipt for proof.

- PriorTax can automatically prepare your Form 843 Kwong protective claim before the July 10, 2026 deadline.

Tens of millions of taxpayers may qualify for an IRS COVID penalty refund and not realize it.

A federal court ruling in late 2025 changed how the COVID-19 disaster period affects penalties and interest assessed between January 20, 2020 and July 10, 2023.

Under that ruling, the IRS should not have charged failure-to-file penalties, failure-to-pay penalties, estimated tax penalties, or related interest during that 3.5-year window.

The catch? You have to ask for the money back.

Relief is not automatic, and the deadline to file a claim is July 10, 2026.

If you filed late for tax year 2019, 2020, 2021, or 2022, this directly affects you. The same goes for anyone still carrying an unpaid balance from those years.

Here is what happened, who qualifies, and how to file before the window closes.

What the Kwong Ruling Actually Said

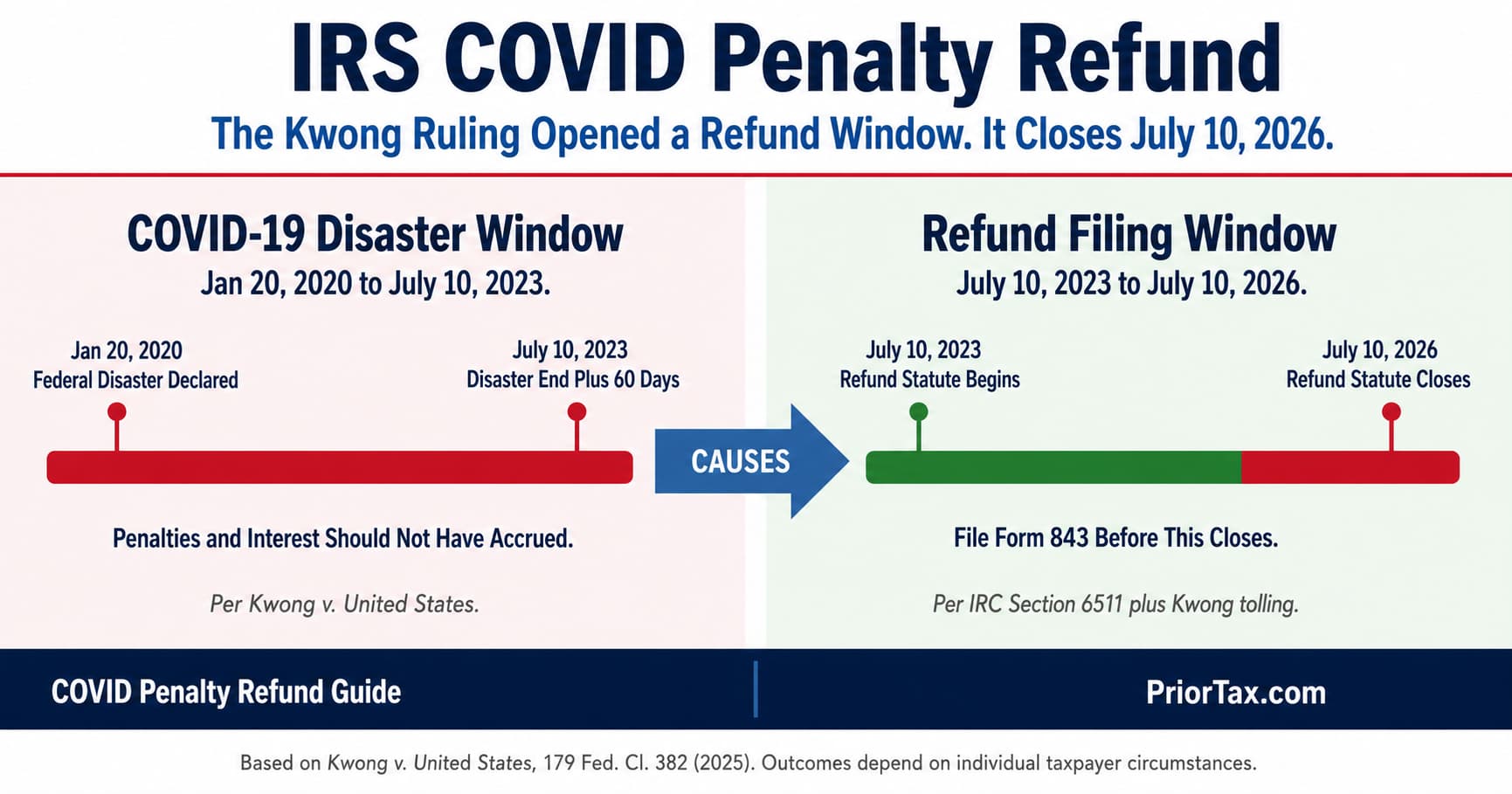

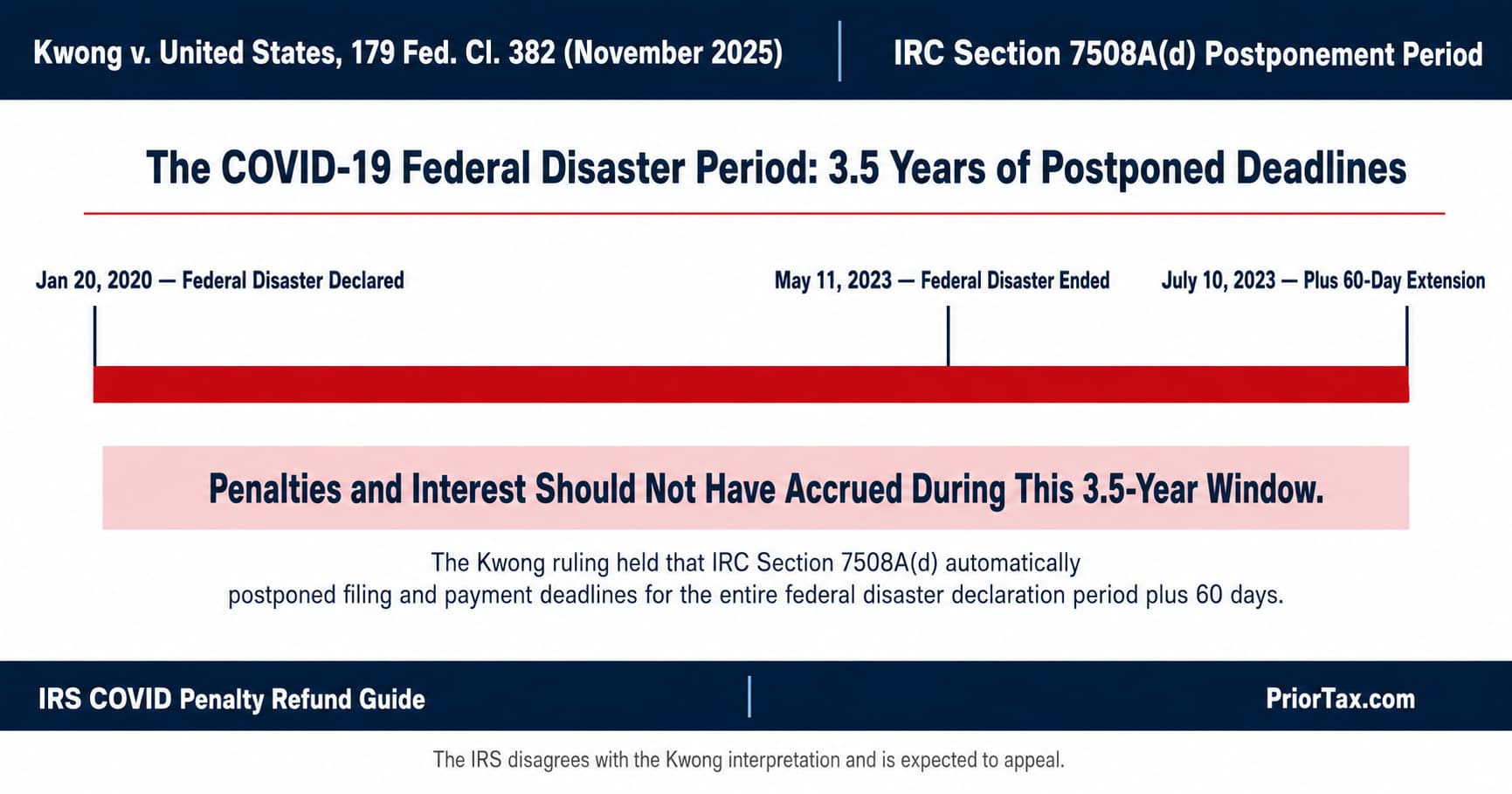

The ruling came down in Kwong v. United States, 179 Fed. Cl. 382 (November 2025). The U.S. Court of Federal Claims looked at a section of the tax code called IRC § 7508A(d), which deals with what happens to filing and payment deadlines during a federally declared disaster.

Here is what the court found. When the COVID-19 federal disaster declaration was in effect, filing and payment deadlines were automatically postponed for the entire duration of the disaster, plus 60 days. That declaration ran from January 20, 2020 through May 11, 2023. Add 60 days and you reach July 10, 2023.

The court’s language was direct: the automatic extension runs from the start of the disaster declaration through 60 days after it ends.

Under that reading, returns and payments due any time within that 3.5-year window were not late until after July 10, 2023.

The IRS, however, treated them as late and charged penalties anyway. The court said that was wrong.

The IRS disagrees with the decision and is expected to appeal. That is exactly why filing a protective claim now matters. You preserve your right to a refund while the courts work it out.

Who Qualifies for an IRS COVID Penalty Refund

The reach of this ruling is wide.

National Taxpayer Advocate Erin Collins called it a “broad cross-section of the public,” including individuals, small businesses, large corporations, estates, and trusts.

For most readers of this article, the qualifying group breaks down into two clear buckets.

Bucket one: you already paid penalties or interest assessed during the disaster window. You filed late or paid late for these tax years: 2019, 2020, 2021, or 2022. The IRS charged you a failure-to-file penalty, a failure-to-pay penalty, or interest. You paid it.

Under Kwong, you can ask for that money back as a refund.

Bucket two: penalties were assessed but you have not paid them yet.

Maybe you got a penalty notice. Maybe you set up an IRS payment plan and you are still working through the balance. Maybe the amount sits in active collections.

Under Kwong, you can ask the IRS to abate (remove) what you have not paid yet.

The same Form 843 handles both situations. The language inside the form changes slightly, but the deadline and process are the same.

One more group worth flagging: anyone hit with an estimated tax penalty under IRC § 6654 during this period. That penalty often catches self-employed taxpayers and gig workers off guard.

If the underlying payment deadlines fell inside the disaster window, the penalty may qualify too.

How Much Could You Get Back

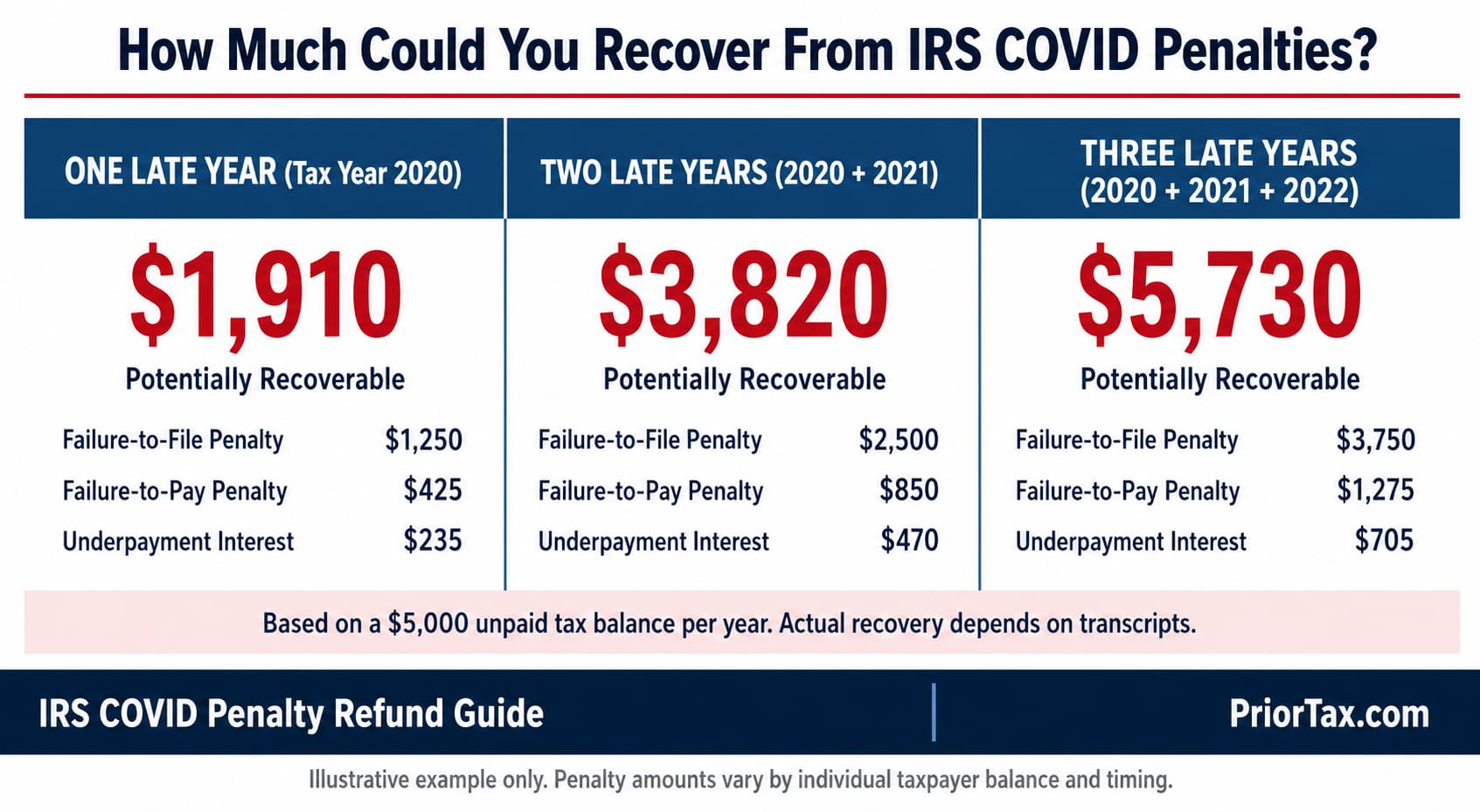

The numbers add up faster than most people expect.

The IRS failure-to-file penalty runs 5% of unpaid taxes per month, capped at 25%. The failure-to-pay penalty adds another 0.5% per month, also capped at 25%. Interest compounds daily on top of both.

Run the math on a real example.

Say you filed your 2020 return 10 months late with a $5,000 balance due. The failure-to-file penalty maxes out at $1,250 (25% of $5,000). The failure-to-pay penalty adds roughly $250. Interest during that period might add another $200 to $400, depending on the rate cycles.

That is over $1,700 in penalties and interest on a single tax year. Stack two or three late years together and the recoverable amount can clear $5,000 fast.

During fiscal year 2023 alone, the IRS assessed more than 14.2 million individual estimated tax penalties and roughly 18.6 million failure-to-pay penalties.

The pool of potentially recoverable dollars is enormous.

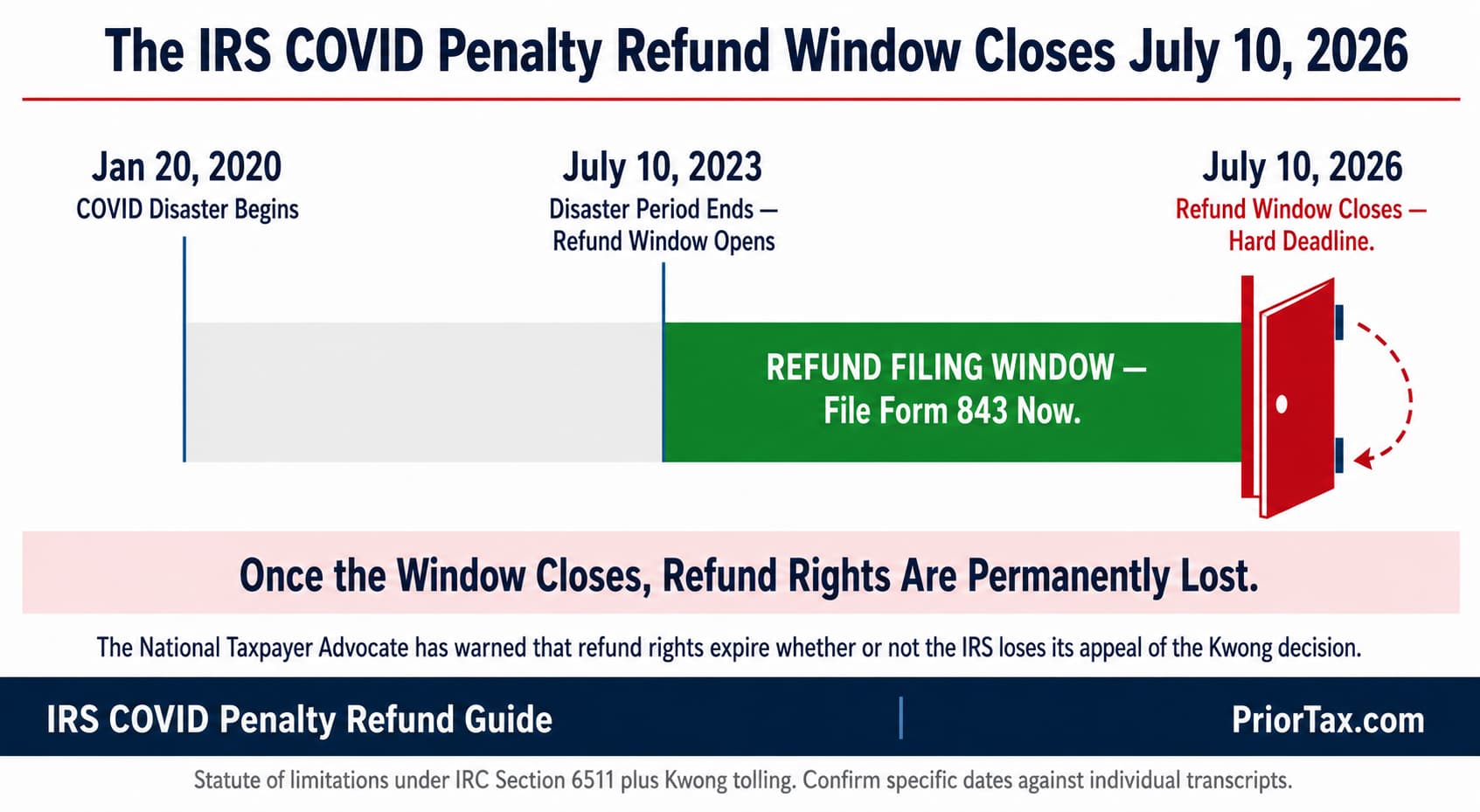

The July 10, 2026 Deadline Explained

July 10, 2026 is not arbitrary.

It is exactly three years from the extended deadline of July 10, 2023 that the court recognized as the end of the COVID disaster postponement period.

The general rule under IRC § 6511 gives taxpayers three years from the filing deadline (or two years from the date the tax was paid, whichever is later) to claim a refund.

Three years from July 10, 2023 lands on July 10, 2026.

Miss the deadline and the statute of limitations closes. Permanently. Even if the IRS loses the appeal and the law is finally settled in the taxpayer’s favor, you cannot collect on a claim you never filed.

This is why the National Taxpayer Advocate has been so vocal. She has warned that without action, the “well advised” will receive refunds and the “unaware” will lose their rights entirely.

That is not how the tax system is supposed to work.

How to File a COVID Penalty Refund Claim Using Form 843

The process is paperwork-heavy but straightforward.

Six steps.

Step one: pull your IRS account transcripts. Log into your IRS.gov online account and request account transcripts for tax years 2019 through 2022. The transcripts show every penalty and interest charge assessed to your account, with dates.

Step two: identify the qualifying assessments. Look for any failure-to-file penalty, failure-to-pay penalty, estimated tax penalty, or interest charge with an accrual date between January 20, 2020 and July 10, 2023. Flag those amounts.

Step three: download Form 843, Claim for Refund and Request for Abatement, from IRS.gov. Print it. There is no e-file option for this form.

Step four: fill out the form. Across the top, write “Protective Refund Claim Pursuant to Kwong Case” exactly as written. That phrase is what makes it a protective claim and locks in your right to a refund while the appeal plays out. List the tax year, the type of penalty or interest, the amount, and a brief statement citing IRC § 7508A(d) and the Kwong decision as the legal basis.

Step five: prepare a separate Form 843 for each tax year. If you have penalties from 2020 and 2021, that is two forms, not one. You can mail them together, but they have to be filled out separately.

Step six: send by certified mail with return receipt requested. This gives you documented proof of timely filing if the IRS ever loses or misplaces your paperwork. Keep the receipt and the green card in a safe place. The mailing address depends on the type of tax involved and is listed in the Form 843 instructions.

Protective Claim vs. Standard Refund Claim

A standard refund claim asks for a specific dollar amount back.

A protective claim preserves your right to a refund while the underlying legal question is still being decided.

The IRS recognizes protective claims under IRM 25.6.1.10.3.2.5(2). The claim must identify the taxpayer, the tax year, the legal basis, and the nature of the relief requested. It does not need to nail down the exact refund amount up front.

Why does this matter?

Because the Kwong decision is being appealed.

If you file a regular refund claim today and the IRS denies it based on its current position, you would normally have only two years to sue. A protective claim sits in administrative suspense until the courts settle the issue, then gets “perfected” with final numbers once the law is clear.

One more thing. Protective claims also work for abatement requests on penalties you have not paid yet.

The mechanism is the same. The form is the same. Only the relief requested changes.

What to Do If You Have Not Filed Those Returns Yet

Here is the part most articles miss.

To claim a Kwong refund, you generally need to have actually filed the return for the year in question. If you never filed your 2020 or 2021 return, you have a more pressing problem to solve first.

Filing late returns is solvable. It is what PriorTax does.

The platform supports prior-year filing for tax years 2012 through the current year, with e-file available for the current year and the three most recent prior years. Older years print and mail.

If a tax return was never filed at all, the three-year refund window measures from the date the return was filed, not from the original due date. Filing now starts the clock. Waiting longer can close the window on any refund the return itself might have generated, separate from the Kwong issue.

The two issues stack.

Get the return filed, then file the Form 843 for any penalties tied to that year.

Both deadlines run in parallel, but the Kwong claim deadline of July 10, 2026 is the harder backstop.

Common Mistakes That Could Cost You the Refund

- Trying to e-file Form 843. The IRS does not accept this form electronically. It has to be paper.

- Filing one Form 843 for multiple tax years. Each year needs its own form.

- Using regular mail instead of certified mail with return receipt. Without proof of mailing, a lost claim is your problem, not the IRS’s.

- Skipping the “Protective Refund Claim Pursuant to Kwong Case” header language. Without that phrase, the IRS may not treat it as a protective claim.

- Waiting for the IRS to send you a notice. They are not going to. The National Taxpayer Advocate has been clear that this relief will not happen automatically.

- Filing a claim for a year where you never actually filed the underlying return. Get the return in first.

What Happens Next

The Department of Justice is expected to appeal the Kwong decision to the Federal Circuit.

That process could take years.

In the meantime, the IRS may grant claims, deny them, or hold them in suspense pending the final outcome.

If your claim is denied outright, you typically have two years to file suit in federal district court or the U.S. Court of Federal Claims. If it is held in suspense, you wait.

Either way, your protective claim preserves your seat at the table.

The IRS has not announced any systemic relief program. The National Taxpayer Advocate has asked the agency to consider one, along with an electronic filing option and a six-month deadline extension.

None of that has materialized. The current process is what it is.

Frequently Asked Questions

Is the IRS automatically refunding COVID-era penalties?

No. The IRS is appealing the Kwong decision and has not begun issuing refunds. The National Taxpayer Advocate has confirmed that relief will not happen automatically. You must file Form 843 by July 10, 2026 to preserve your claim.

Can I file Form 843 online?

No. Form 843 must be filed on paper and mailed to the IRS. There is no electronic filing option as of May 2026. The National Taxpayer Advocate has asked the IRS to build one, but it does not exist yet.

Do I need a tax professional to file a Kwong refund claim?

Not technically. The form itself is short. But the legal basis, the math, and the protective claim language need to be right. For larger penalty amounts or multi-year situations, a tax professional can help confirm eligibility and tighten the claim.

What if I already paid my COVID-era penalties years ago?

You can still file. The refund statute of limitations under IRC § 6511 gives you the later of three years from the filing deadline or two years from the date the tax was paid. Under Kwong, the COVID postponement period gets disregarded in that calculation, which is what extends the window to July 10, 2026 for most taxpayers.

What if I am still in IRS collections for those years?

That actually makes filing a Kwong claim more valuable, not less. Penalties and interest assessed during the disaster window can potentially be abated, reducing what you owe. File the Form 843 as a protective claim, and raise the Kwong issue in any collection due process proceeding you have open.

Does this apply to state tax penalties?

No. The Kwong decision interprets federal tax law under IRC § 7508A(d). State tax penalties follow state law and are not covered by this ruling. If you live in a state with income tax, check your state’s separate rules.

The Bottom Line

July 10, 2026 is the date that matters.

If you filed late or got hit with IRS penalties for any tax year between 2019 and 2022, the Kwong ruling may have opened a window to recover that money. The IRS is not going to call you. The window does not extend on its own.

Pull your transcripts. Identify the qualifying assessments.

Fill out Form 843 with the “Protective Refund Claim Pursuant to Kwong Case” header language.

Mail it certified before July 10, 2026.

For taxpayers who still need to file the underlying returns for 2020, 2021, or 2022 first, PriorTax handles prior-year filings at a flat, transparent price with expert review on every return.

Getting current is the first step. The Kwong claim is the second.

Categories: