Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments May 1, 2026

May 1, 2026Key Takeaways

- File every unfiled tax return before pursuing an installment agreement, penalty abatement, or Offer in Compromise

- Choose an IRS installment agreement when you owe taxes but can manage the balance through monthly payments

- Request penalty abatement or an Offer in Compromise only after filing all returns and documenting financial hardship

- Act on every IRS notice before the deadline — ignored notices accelerate enforced collection, liens, and wage garnishment

- PriorTax helps taxpayers file missing returns and navigate back tax resolution with affordable, transparent pricing

A tax bill you cannot pay feels urgent because the clock starts running fast.

Understanding what happens if you don’t pay taxes helps you separate immediate damage from long-term risk and pick the least expensive path forward.

Start Here: Not Filing vs. Not Paying

Two different problems create two different kinds of trouble: failing to file a return on back taxes and failing to pay the tax balance due.

The Internal Revenue Service treats unfiled tax returns more harshly in many cases because the agency cannot verify your deductions, tax credits, or actual liability until a return exists.

File on time even if you cannot pay in full.

IRS rules generally make the failure-to-file penalty steeper than the failure-to-pay penalty, so filing can reduce penalties and interest while preserving your ability to request tax payment options.

Deadlines matter immediately. Interest on unpaid taxes and many penalties usually begin around the original due date of the return, not when the IRS finally contacts you.

If You Don’t File, the IRS May Estimate Your Tax

The IRS can prepare a Substitute for Return, often called an SFR, using income documents such as Forms W-2 and 1099. An SFR often produces a higher bill because it may exclude deductions, filing status benefits, and tax credits you could have claimed on your own return.

That difference is not technical trivia.

A taxpayer who files an accurate replacement return can sometimes cut an inflated SFR balance by restoring missing deductions and credits the IRS never included.

If You File but Don’t Pay, Collection Starts With Notices

Filing without payment usually triggers a series of tax notice letters showing the amount due, added penalties and interest, and the next collection stage.

IRS collection typically escalates over time, but early response keeps more options open and lowers the chance of enforced collection.

Even a partial payment helps (even filing years later).

Paying something can reduce the unpaid balance that drives the failure-to-pay penalty and interest calculations.

Immediate Financial Costs: Interest and IRS Penalties

Unpaid taxes gets more expensive every month because interest accrues until the balance is fully paid.

The IRS updates interest rates quarterly, which means back taxes can grow faster than many people expect during periods of higher rates.

The failure-to-pay penalty generally applies when tax is not paid by the due date. When both filing and payment are late, civil tax penalties can stack, so a missed return and an unpaid bill often create a more expensive problem than either issue alone.

States can add their own charges.

A federal balance does not block a state tax agency from imposing separate late filing penalty or late payment penalty rules on the same taxpayer.

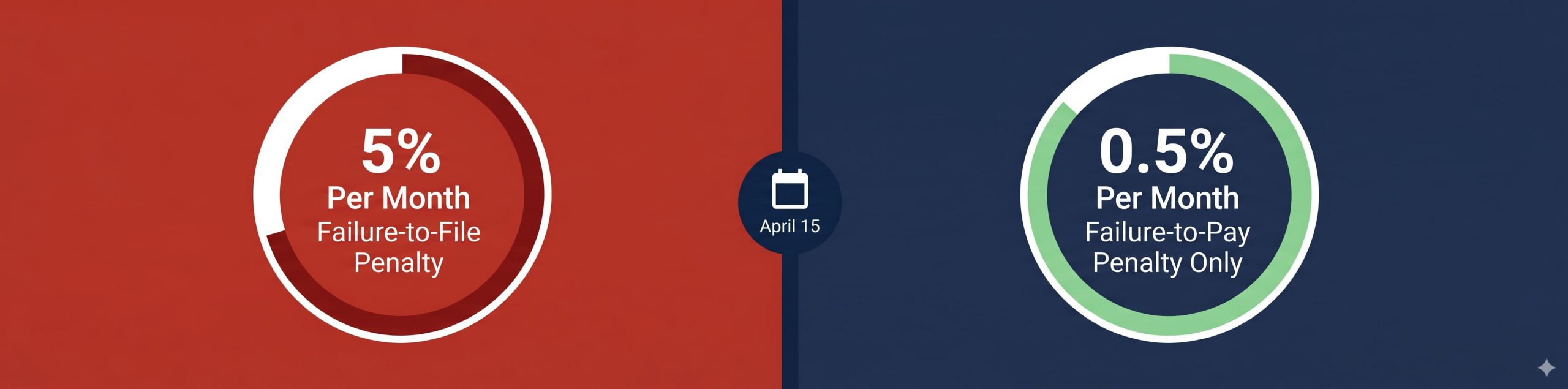

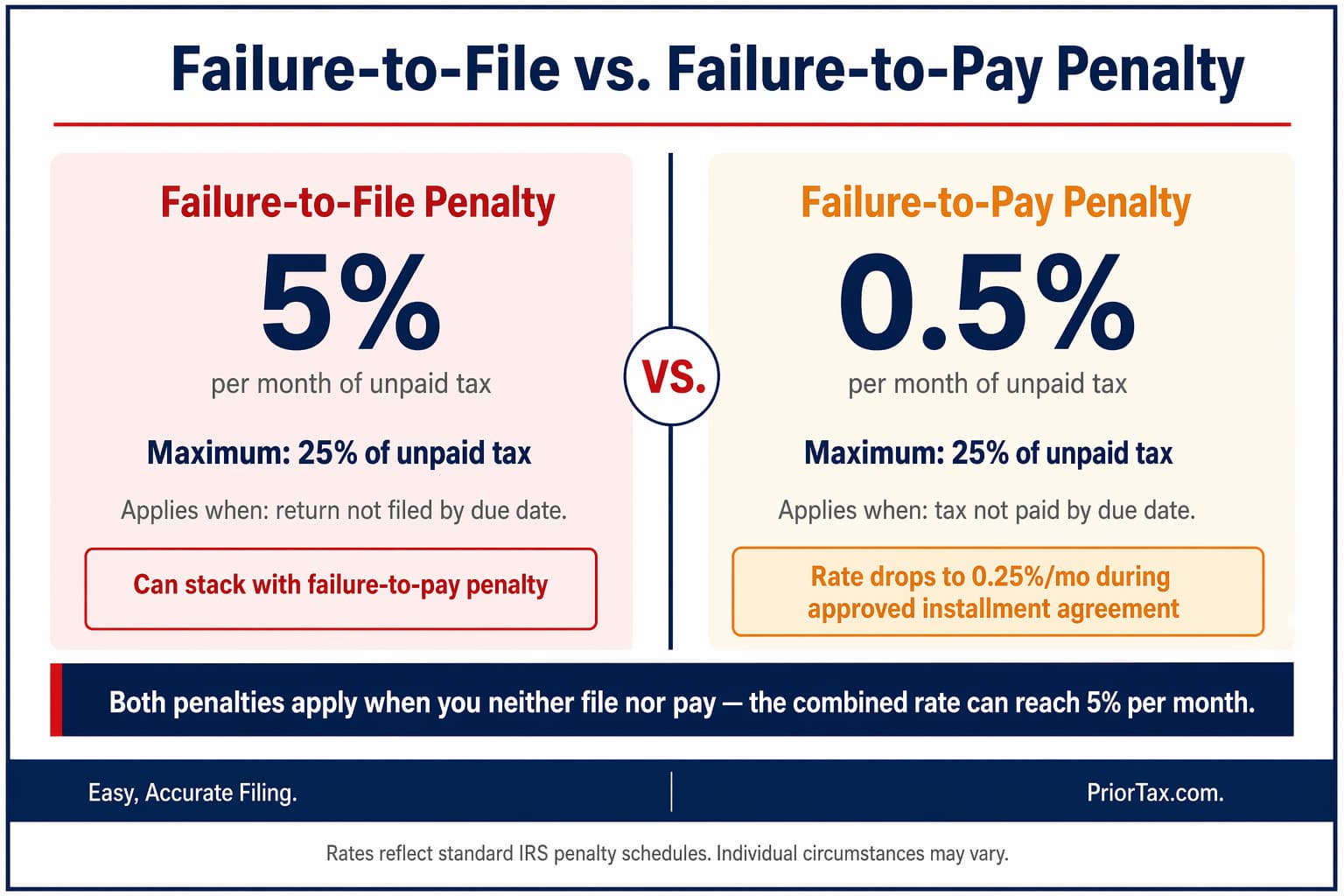

Failure-to-Pay Penalty Basics

IRS guidance states that the failure-to-pay penalty applies when you do not pay the tax shown on your return by the due date.

The common rate starts at 0.5% of the unpaid tax per month, though it can change based on collection status, approved plans, or other circumstances.

That monthly percentage sounds small until it compounds with interest on unpaid taxes. A modest tax balance due can become materially harder to clear if you wait several filing seasons.

Failure-to-File Penalty Can Be Larger Than Failure-to-Pay

The IRS commonly sets the failure-to-file penalty at 5% of unpaid tax per month, up to 25%, according to IRS instructions and penalty guidance.

That structure explains the practical rule tax professionals repeat: file even if you cannot pay.

A filed return narrows uncertainty. An unfiled year leaves room for an SFR, missed refund claims, and fewer relief options later.

State Tax Penalties Can Apply Too

State departments of revenue use their own penalty schedules, deadlines, and collection rules. California Department of Tax and Fee Administration (CDTFA), for example, publishes penalty rules for certain state-administered taxes, which shows that state tax debt can escalate independently from federal debt.

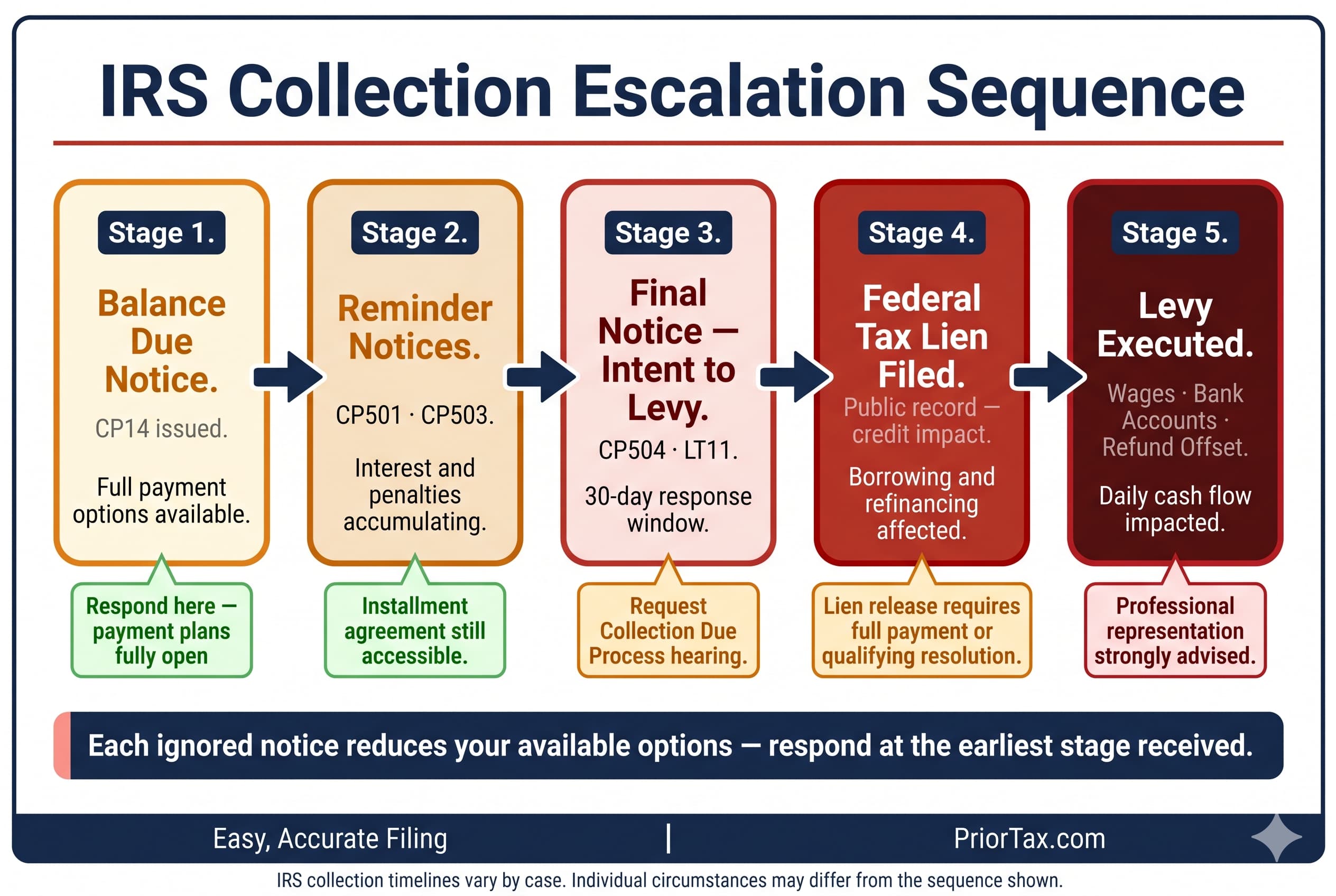

What the IRS Can Do If You Keep Ignoring the Balance

IRS collection usually follows a sequence: bills, stronger notices, final warnings, then enforced collection.

That progression matters because each ignored tax notice reduces your room to dispute the balance, request relief, or stop a levy before money leaves your account.

A tax lien and a tax levy are not the same thing. A lien is a legal claim against property, while a levy is the actual seizure of money or assets.

Tax Lien: Public Claim Against Your Property

A federal tax lien attaches to your property and rights to property when tax is assessed and remains unpaid after demand for payment.

That claim can complicate refinancing, business borrowing, or asset sales because lenders and buyers care about priority rights.

Release usually requires paying the debt, settling it under IRS rules, or otherwise meeting release criteria. The practical impact is credit and financing friction, not just paperwork.

Tax Levy: Taking Money From Wages or Accounts

A tax levy reaches actual assets, including wages and bank funds, after required notices and waiting periods.

Wage garnishment sends part of each paycheck to the IRS, while a bank levy freezes and can remove money already sitting in the account.

Early contact often prevents this stage.

Once levy action starts, daily cash flow becomes the problem, not just the tax bill.

Refund Offsets and Other Collection Tools

The IRS can apply a future tax refund to older unpaid balances through a refund offset.

The agency may also apply payments and refunds to existing liabilities under its own ordering rules, which can affect how quickly a specific tax year is resolved.

Can You Go to Jail for Not Paying Taxes?

Most unpaid tax cases stay civil, not criminal.

Penalties, liens, levies, and installment agreement negotiations are the normal tools when someone owes money but is not committing fraud.

Criminal tax charges usually involve willful conduct such as tax evasion, false documents, or deliberate concealment of income. Good-faith filing, recordkeeping, and communication with the IRS help show the difference between inability to pay and intentional misconduct.

Civil vs. Criminal: What Usually Triggers Criminal Charges

Red flags include falsified records, hidden bank accounts, nominee ownership, intentional non-filing over multiple years, and false statements to the government.

The Department of Justice Tax Division and the IRS Criminal Investigation unit focus on conduct that shows intent, not simple financial distress.

Most people who file returns and work on a resolution remain in the civil system. That is why documentation matters.

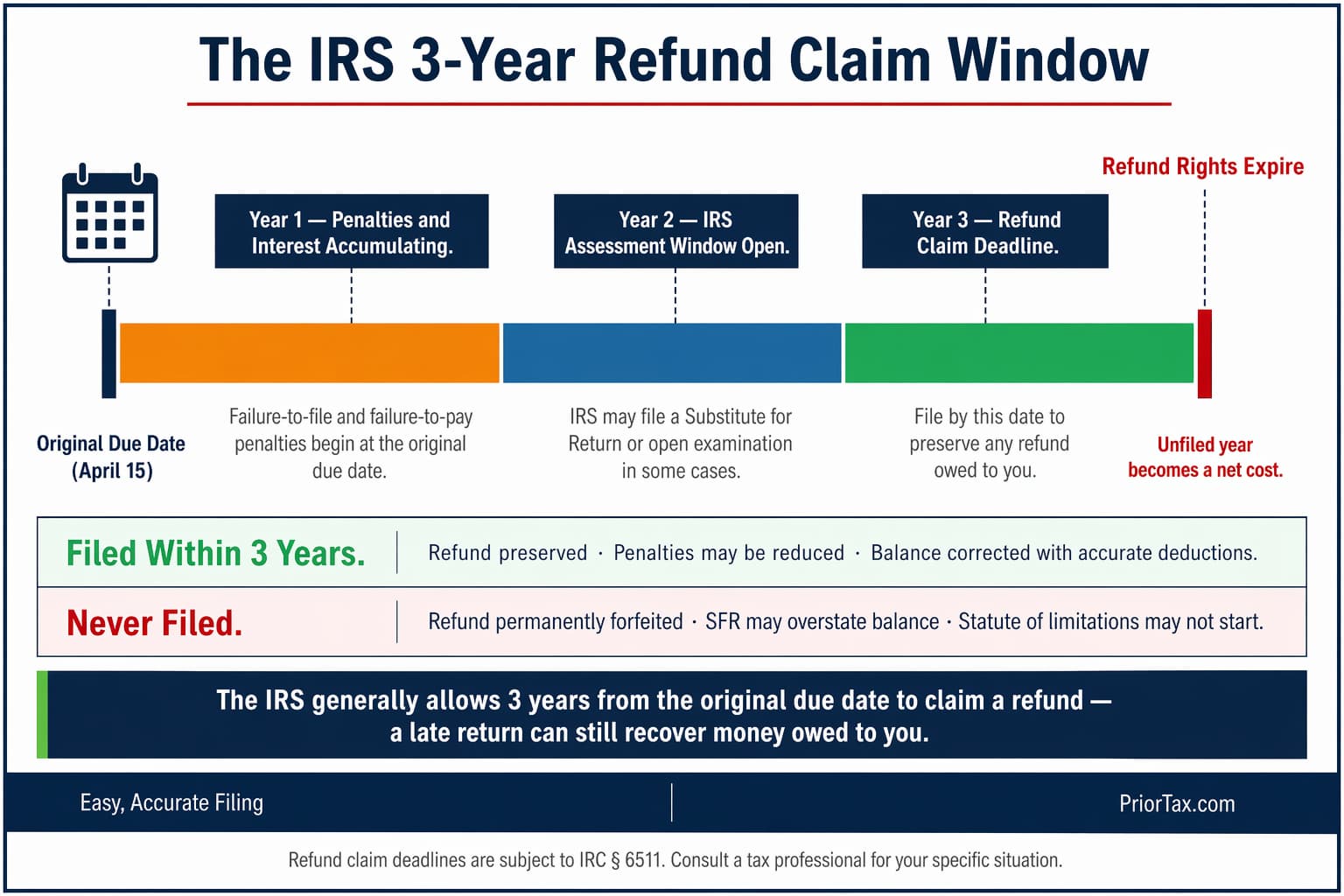

How Long Can You Go Without Paying or Filing?

The longer a balance sits unresolved, the more expensive and restrictive it becomes.

Waiting increases penalties and interest, raises collection risk, and can block access to relief programs that require all required returns to be filed first.

Time limits also work differently when no return exists. Certain statute of limitations rules depend on a filed return, so unfiled tax returns can leave the government with more room to assess tax.

No Return Filed Means Fewer Time Limits to Help You

A filed return often starts important clocks for assessment and collection rules.

Without that filing, some limitation periods may not begin in the same way, which is one reason old unfiled years remain dangerous.

Catch up before seeking relief.

Payment plans, penalty abatement requests, and Offer in Compromise reviews usually work better when missing years are already filed.

Refund Window: You Can Lose Money by Waiting

Refund rights do not last forever.

The IRS generally gives taxpayers three years from the original due date to claim a tax refund, so delay can turn a refundable year into a lost year.

That rule changes the math for back taxes. Late filing is not only about avoiding penalties; it can also preserve money owed back to you.

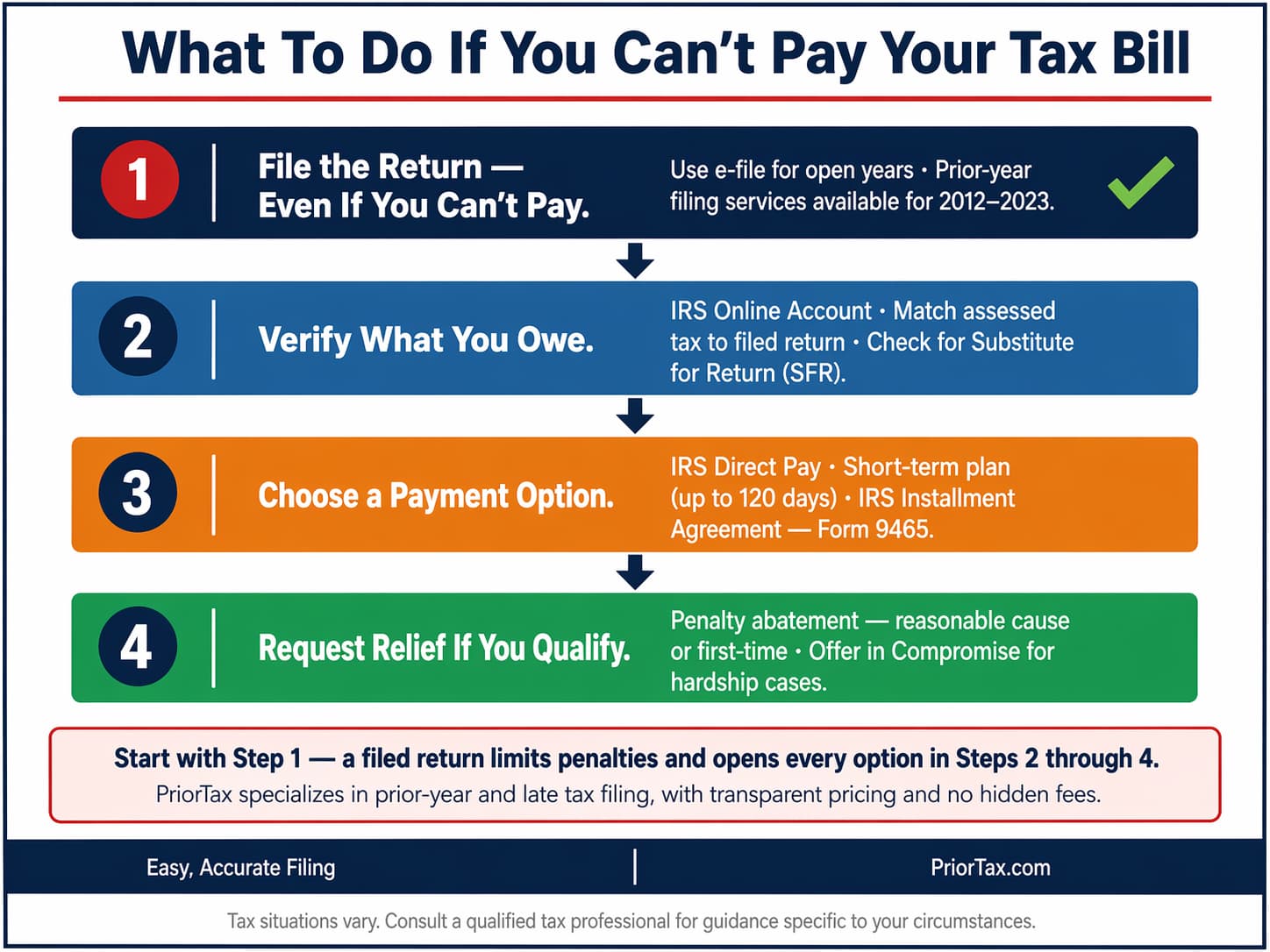

Step-by-Step: What To Do If You Can’t Pay Your Tax Bill

Start with the return, not the payment plan.

A filed return establishes the real balance, limits some penalties, and gives the IRS a current record to work from.

Then verify the numbers, choose a payment path, and act before enforced collection begins.

This sequence works for W-2 employees, freelancers, and self-employed taxpayers alike.

Step 1: File the Return (Even If You Can’t Pay)

Use e-file for open years when available, and submit each prior-year return that is still missing. If you need older forms, services like PriorTax that help taxpayers file 2024 taxes, 2023 taxes, or can help reconstruct even older filings.

A return beats an estimate.

It replaces uncertainty with documented numbers.

Step 2: Verify What You Owe in an IRS Online Account

An IRS online account shows assessed tax, penalties and interest, payment history, and some notice details. Match those records against your filed return so you do not pay the wrong amount or miss an SFR-based assessment that should be corrected.

Step 3: Choose a Payment Option That Fits Your Cash Flow

IRS tax payment options include short-term arrangements, a long-term IRS installment agreement, and direct payments through IRS Direct Pay.

Fees may apply to some plans, but an affordable installment agreement is often cheaper than waiting for levy action.

Step 4: Ask for Relief When You Qualify

Penalty abatement may be available for reasonable cause or certain first-time situations.

An Offer in Compromise can settle tax debt for less than the full amount in hardship cases, but it is not a default shortcut and requires detailed financial disclosure.

Examples: What Nonpayment Can Look Like in Real Life

A taxpayer files on time, owes $4,000, and cannot pay by April.

Interest and the failure-to-pay penalty begin, but partial payments plus an installment agreement prevent levy risk and keep the case in routine IRS collection.

Another taxpayer skips filing for three years.

The IRS creates an SFR, ignores available deductions, and assesses a larger bill than necessary until accurate returns replace the estimates.

State problems can escalate separately. A business with unpaid sales tax may face action from a state agency even while resolving federal income tax debt, which is why early contact matters on both fronts.

Scenario A: Filed on Time, Couldn’t Pay the Balance

This taxpayer avoids the larger late filing penalty by filing on time. Each payment reduces the principal that drives future penalties and interest.

Scenario B: Didn’t File for Multiple Years

The SFR raises the bill because it usually omits tax credits and favorable filing positions. Filing correct returns can replace the SFR and lower the assessed amount.

Scenario C: Business Sales Tax or State Agency Debt

State agencies can assess and collect separately from the IRS. Fast filing and direct contact may open payment plans or penalty relief before collection hardens.

Common Mistakes That Make Tax Debt Worse

Ignoring IRS letters is expensive because deadlines control appeals, payment plans, and levy prevention.

A missed notice deadline can move a case from manageable to urgent without changing the underlying tax by much.

Skipping filing because you cannot pay is another costly mistake. A tax extension also causes confusion because many taxpayers think extra filing time means extra payment time.

Treating an Extension as a Payment Delay

Form 4868 gives an extension to file, not an extension to pay. If you need a tax extension, make an estimated tax payment by the deadline to reduce penalties and interest.

Not Tracking Notices, Deadlines, and Documentation

Keep a simple log of each notice, phone call, upload, and payment confirmation. Good records help a CPA, Enrolled Agent, or tax attorney fix problems faster and cut billable time.

When to Get Professional Help

Professional help makes sense when the facts get layered: several unfiled years, a levy notice, a large balance, or business payroll tax exposure.

Early intervention often prevents enforced collection that becomes harder and costlier to reverse.

A CPA usually focuses on returns and financial analysis, an enrolled agent is federally authorized to represent taxpayers before the IRS, and a tax attorney is strongest when legal exposure or litigation risk exists.

Bring notices, transcripts, prior returns, and income records before the first call.

Signals You Should Not Handle It Alone

Wage garnishment, bank levy risk, an SFR already on file, or payroll tax issues are strong signals to get help.

Those facts usually mean the case has moved beyond simple catch-up filing.

Practical Wrap-Up: The Fastest Way to Limit Damage

File every missing return, confirm the balance, and respond before the IRS moves from notices to action. Most damage comes from delay, not from the first bill.

One-Page Action Checklist

File all missing returns and any prior-year return still outstanding.

Check your IRS online account, pay what you can through IRS Direct Pay, request an installment agreement or other relief if needed, and keep copies of every notice and payment receipt.

Frequently Asked Questions (FAQs)

What happens if you just never pay taxes?

Unpaid tax usually keeps growing through penalties and interest. The IRS can escalate from notices to liens, levies, wage garnishment, bank levy action, and refund offset.

What is the punishment for not paying taxes?

Most cases involve civil tax penalties, interest, liens, and levies. Criminal punishment usually requires willful tax evasion, fraud, or deliberate non-filing rather than simply owing money.

What’s the longest you can go without paying taxes?

Waiting increases cost and risk every month. If you do not file, some time limits may not start, and the IRS may assess tax through a Substitute for Return that overstates what you owe.

What happens if I owe the IRS and can’t pay?

File the return first, pay what you can, and confirm the balance in your IRS Online Account. Then review tax payment options such as an IRS installment agreement, penalty abatement, or an Offer in Compromise if hardship applies.

Categories: