Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments Apr 30, 2026

Apr 30, 2026**updated 6-19-2026

Key Takeaways

- IRS failure-to-file penalty is usually 5% of unpaid tax per partial month.

- Late-payment penalties usually add 0.5% monthly, while daily compounding interest keeps growing.

- Form 4868 extends filing time, but tax due can still trigger penalties and interest.

- Refund claims usually avoid late-filing penalties, but the three-year refund rule can erase refunds.

- PriorTax helps hard-working taxpayers maximize refunds and pay less to file accurately.

Missed the tax deadline and worried about what the Internal Revenue Service will do next?

Most taxpayers run into trouble with the penalty for filing taxes late only when they owe a balance due, because the IRS treats a late tax return and a late payment as separate compliance failures.

This guide explains how federal income tax penalties work when you miss the deadline, what keeps growing after the deadline, how state income tax rules can differ, and what steps cut the damage fastest.

What Happens When You File After the Deadline

The IRS usually looks at two separate issues: whether you filed the tax return on time and whether you paid the tax due on time.

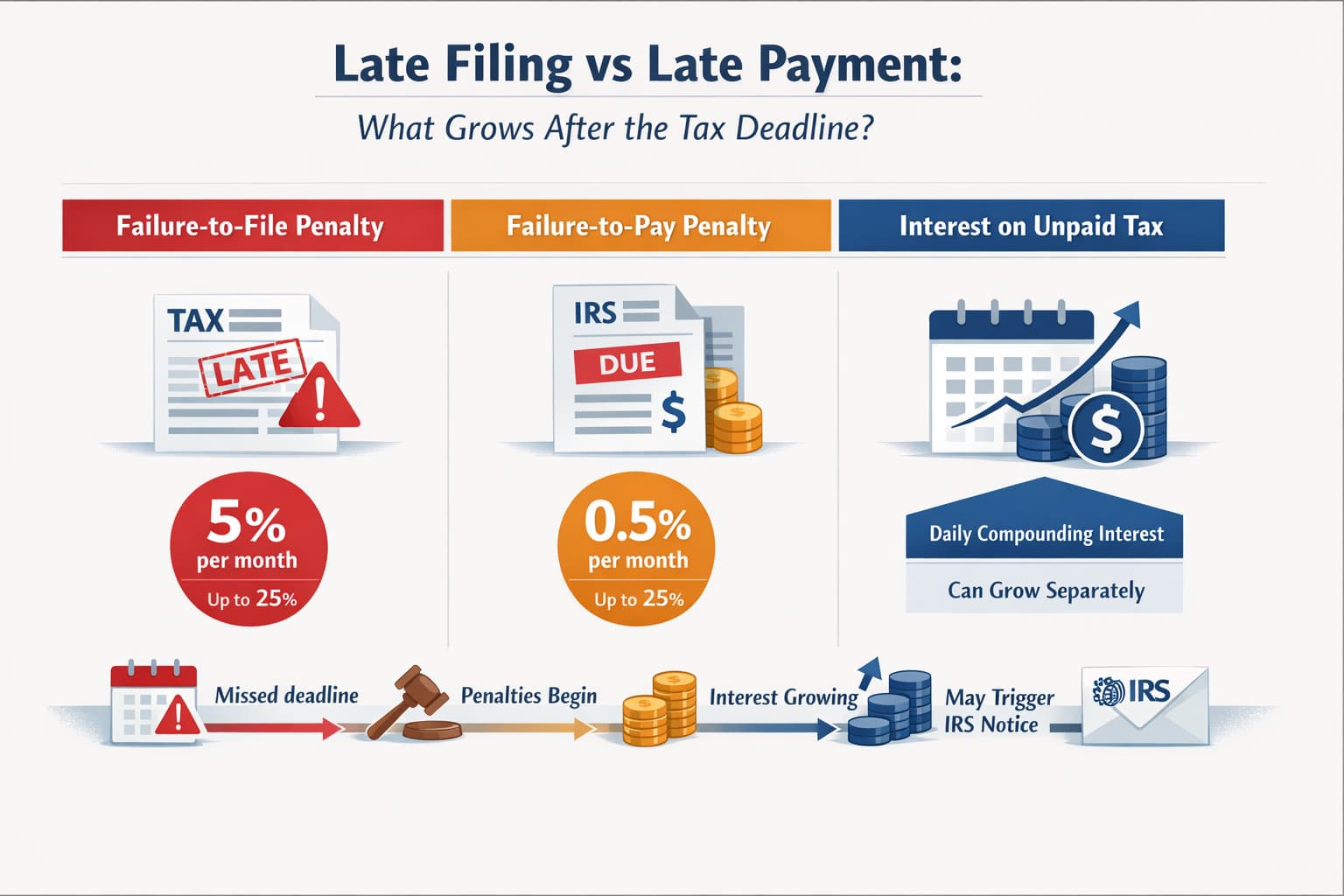

That distinction matters because the failure-to-file penalty is usually steeper than the failure-to-pay penalty, which means filing late often costs more than paying late.

Most late-filing problems start when a taxpayer owes unpaid tax and misses the filing deadline without a filing extension.

Penalties can accrue for each month or partial month, and interest on unpaid tax generally uses daily compounding interest, so even a short delay can turn a manageable bill into a larger IRS bill.

Federal and state income tax systems do not always match.

A taxpayer can be current with the IRS and still owe separate penalties and interest to a state revenue agency, which is why the actual due date and late rules should be checked for both returns.

If You’re Due a Refund vs If You Owe Taxes

A refund changes the risk profile. If you are due a tax refund, the IRS generally does not charge a failure-to-file penalty, but the three-year refund rule can lead to refund forfeiture if you wait too long to claim it.

Owing money creates the opposite result.

Once a balance due exists, the IRS can assess the failure-to-file penalty, the failure-to-pay penalty, and interest and penalties until the account is resolved.

How the IRS Calculates the Late-Filing Penalty

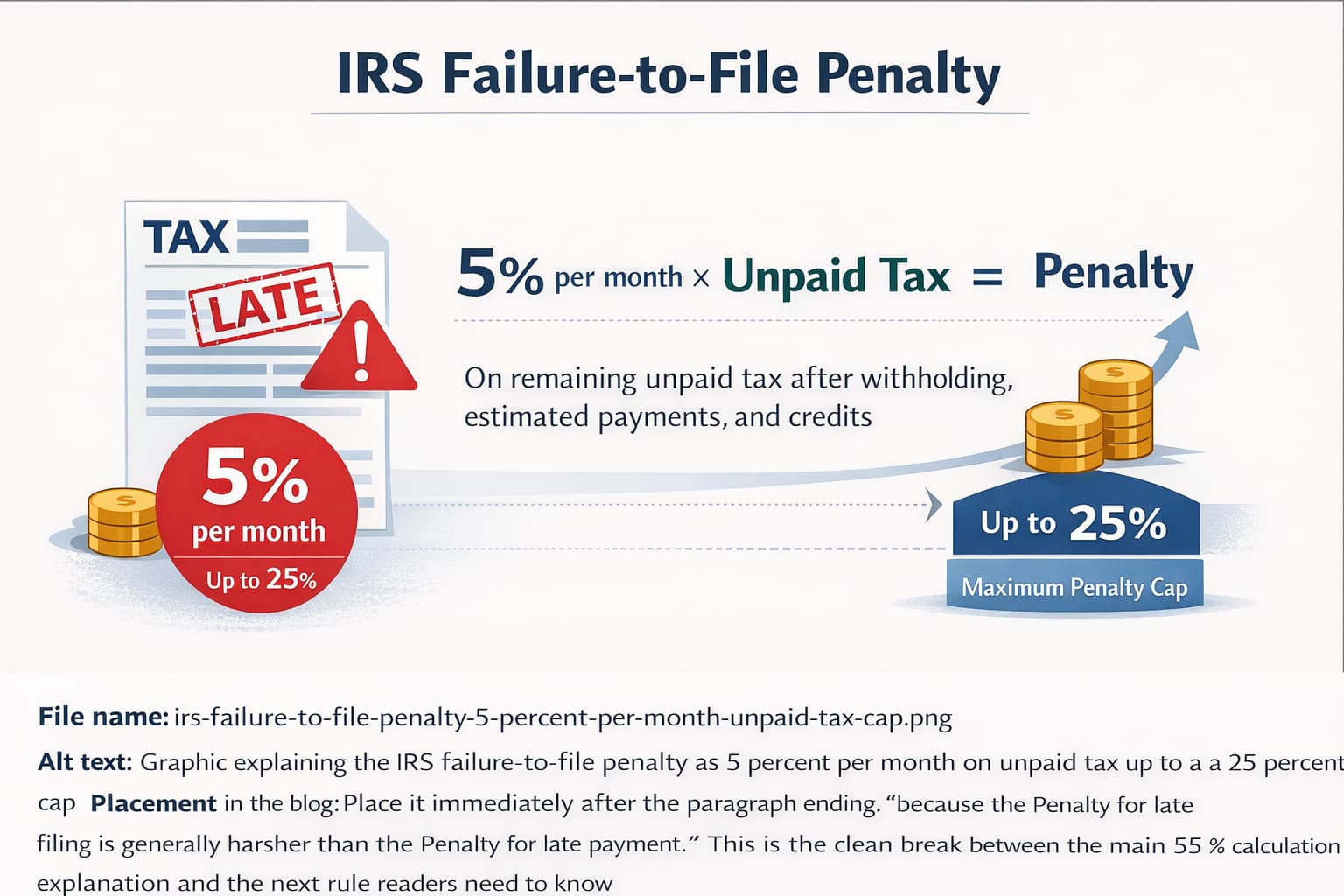

IRS Topic No. 653 explains the standard framework: the failure-to-file penalty is commonly 5% of unpaid tax for each month or partial month that a return is late, up to a maximum penalty cap of 25%. That monthly penalty rate applies to unpaid tax after timely withholding, estimated tax payment amounts, and available tax credits are taken into account.

“Unpaid tax” does not mean your total tax liability in the abstract. It means the remaining federal income tax due after payments and credits already on the account, which is why a well-timed estimated tax payment can reduce the base on which penalties are calculated.

Filing the return even without full payment usually stops the failure-to-file penalty from growing further. That single move often saves more money than waiting until you can pay in full, because the Penalty for late filing is generally harsher than the Penalty for late payment.

The 60+ Days Late Minimum Penalty

A return filed more than 60 days late can trigger a minimum late-filing penalty. The amount can change by tax year, so taxpayers should verify the current figure in IRS guidance before estimating what they owe.

Late Filing vs Late Payment: Which Costs More

Late filing usually costs more than late payment because the failure-to-file penalty rate is much higher. If both penalties apply in the same month, the combined charge is commonly described as capped at 5% per month, which limits overlap but does not stop interest on unpaid tax.

The Late-Payment Penalty and Interest (What Keeps Growing)

The failure-to-pay penalty is commonly 0.5% of unpaid tax for each month or partial month after the deadline, up to 25%. That lower rate matters because it shows why filing now, even without full payment, is often the cheapest first move available.

Interest keeps running separately. The IRS charges interest on unpaid tax and may also charge interest on penalties, and daily compounding interest means balances can increase every day the debt remains unpaid.

Paying something is better than paying nothing. A partial payment reduces the unpaid tax base immediately, which can shrink future penalties and interest even if the account stays open.

IRS interest rates can change by quarter, so exact projections should be checked against current IRS interest guidance. Taxpayers who rely on an old rate often underestimate what a delayed payment will really cost.

How Payment Plans Affect Penalties

An installment agreement can keep a late account from escalating into liens or levies if the taxpayer stays compliant. Interest generally continues until the full balance is paid, but IRS payment options still matter because structure reduces enforcement risk and makes the debt predictable.

Step-by-Step: What to Do If You Missed the Deadline

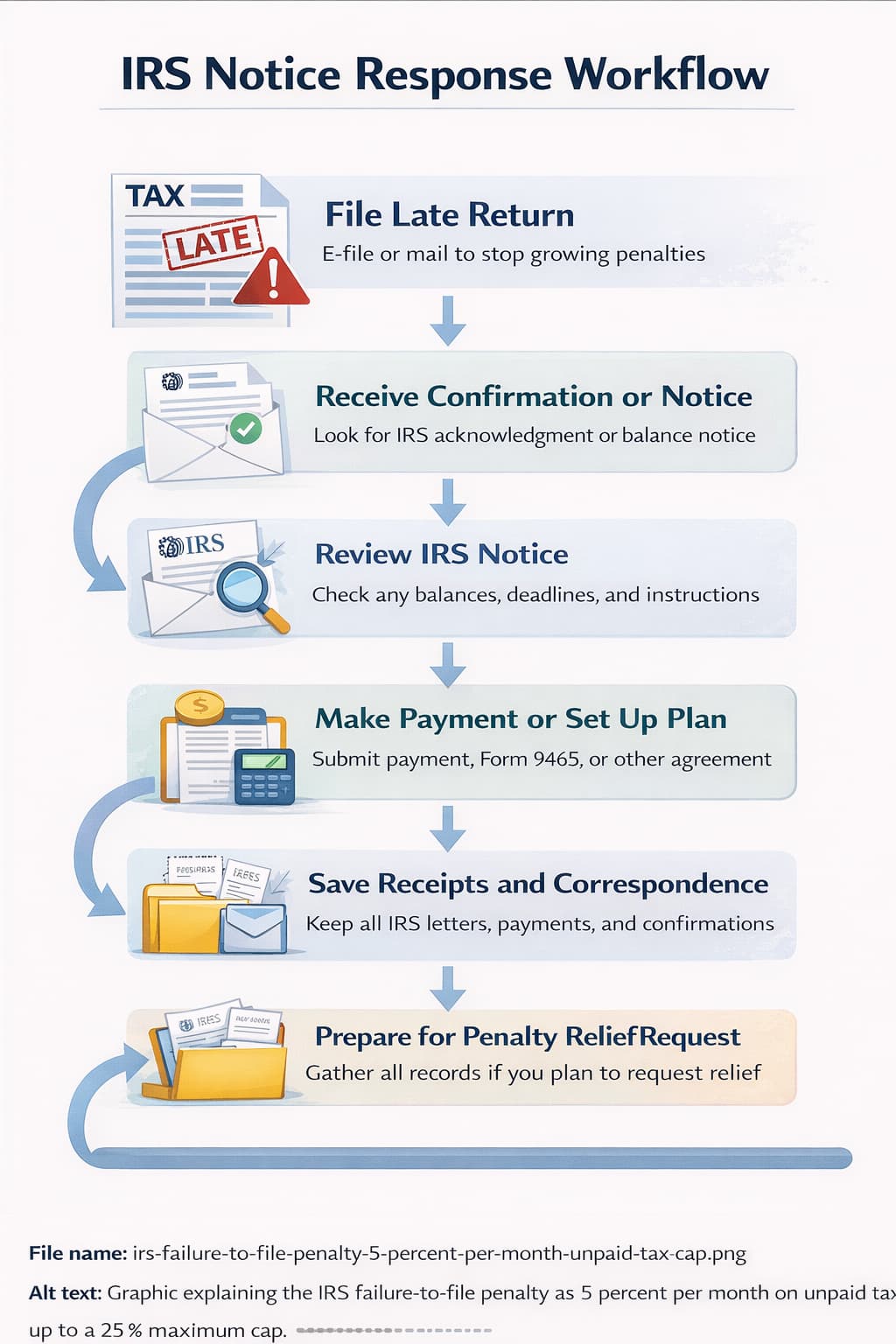

Start by filing the return as soon as possible.

That action limits the failure-to-file penalty, and an e-file confirmation or certified mail receipt gives proof that the IRS received the submission.

Next, pay what you can now, even if the amount feels small. Every dollar applied reduces unpaid tax, which lowers exposure to the failure-to-pay penalty and interest on unpaid tax.

Then choose a resolution path that fits your cash flow. Short-term IRS payment options, an installment agreement request, or a formal request using Form 9465 can prevent the account from drifting into repeated IRS notice cycles.

Keep records. Copies of the filed return, payment confirmations, and every IRS notice create the paper trail you need if the account is misapplied or if you later request penalty relief.

If You Can’t Pay in Full Today

File first. The IRS generally treats nonfiling more seriously than inability to pay, so getting the return on record reduces the most expensive penalty.

An installment agreement is often the next practical step. Taxpayers who need more time can request a payment plan and stay in better standing while the balance is paid down.

If You Haven’t Filed for Multiple Years

Multiple missing returns raise the stakes because the IRS may prepare a substitute for return using income documents it has on file. A substitute for return often ignores deductions and tax credits, which can overstate tax due and produce a larger bill than a properly prepared return.

Start with the oldest required prior-year tax returns and gather W-2s, 1099s, and account transcripts. PriorTax offers options to file previous years of taxes which is useful when old returns still hold refunds or unresolved balances.

How to Avoid Late-Filing Penalties in the Future

A filing extension gives more time to prepare the return, not more time to pay the tax due. That distinction is central because taxpayers who submit Form 4868 but underpay can still face the failure-to-pay penalty and interest.

Estimated payments help. An estimated tax payment made by the original tax deadline reduces unpaid tax, which can cut both penalties and interest if the final return shows a balance due.

Calendar discipline prevents expensive mistakes. Federal deadlines can shift for weekends, holidays, or disaster relief, and state income tax deadlines may not match the federal date.

Records matter more than most people think. Organized receipts, wage statements, and prior-year data reduce filing delays and help taxpayers claim deductions and tax credits correctly the first time.

How a Tax Extension Works (Form 4868 Basics)

Form 4868 generally extends the time to file, not the time to pay. Underpayment after the original deadline can still trigger penalties and interest, so the smartest extension strategy includes a good-faith payment estimate.

Real-World Examples: Quick Penalty Scenarios

Example one: a taxpayer owes $2,000 and files two months late without paying.

A rough estimate of the failure-to-file penalty would be 10% of unpaid tax, or about $200, and the failure-to-pay penalty plus interest would add more.

Example two: a taxpayer is due a refund and files late.

The IRS generally will not assess a late-filing penalty, but the three-year refund rule means the tax refund can be lost permanently if the claim is filed too late.

Example three: a taxpayer files on time but pays late.

That person usually avoids the failure-to-file penalty and deals only with the failure-to-pay penalty and interest, which is why timely filing is such a powerful damage-control step.

Exact numbers depend on the taxpayer’s facts, IRS calculations, and timing. Topic No. 653 gives the framework, but account transcripts and notices control the real balance.

Simple Back-of-the-Envelope Estimate (Not a Quote)

A simple estimate starts with figuring out how many years of unpaid taxes are due. These are multiplied by the monthly penalty rate and the number of months or partial month periods late.

Interest is separate, changes by quarter, and compounds daily, so any quick estimate will understate the final bill if you ignore interest.

Common Mistakes That Make Late Penalties Worse

The costliest mistake is not filing because you cannot pay.

That choice often triggers the larger failure-to-file penalty while doing nothing to stop interest and penalties from building.

Another common error is assuming an extension erases all consequences. A filing extension delays paperwork, not payment, so taxpayers who still owe can receive an IRS bill after the deadline.

Ignoring an IRS notice makes small problems harder to fix. Notices often contain response deadlines, payment options, or correction requests, and missing those windows can lead to stronger collection action.

State returns are easy to overlook. State income tax agencies use their own penalty formulas, so a federal fix does not automatically solve the state side.

Mixing Up “April 15” With the Actual Due Date

April 15 is only a shorthand.

The tax deadline can move because of weekends, legal holidays, or disaster relief, so taxpayers should confirm the exact due date for their filing location and tax year before assuming they are late.

When Penalties May Be Reduced or Removed

Penalty relief is possible, but it is not automatic.

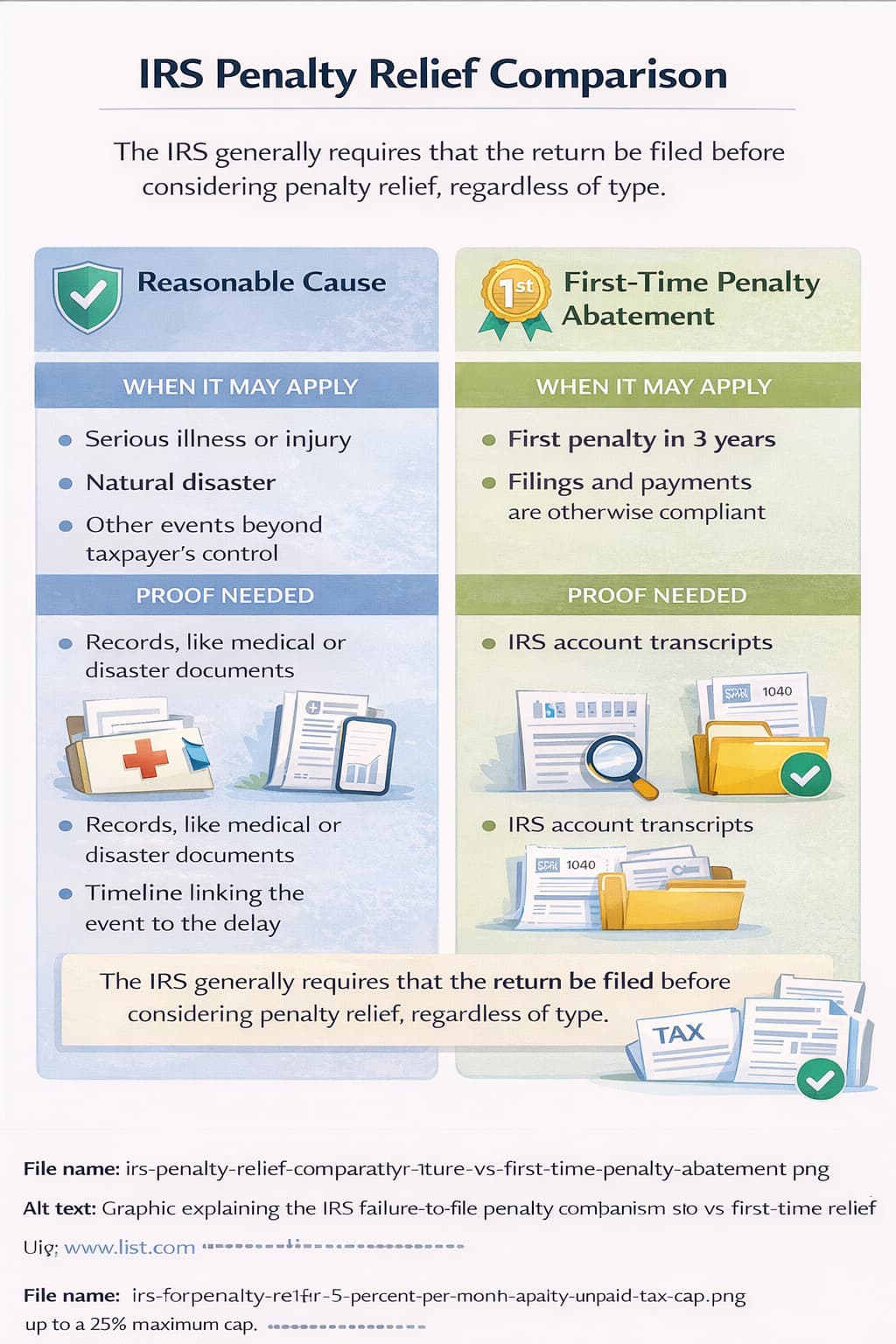

The IRS may remove penalties for reasonable cause when facts show the taxpayer used ordinary business care yet still could not file or pay on time because of events such as serious illness, natural disaster, or records loss.

First-time penalty abatement may also be available for eligible taxpayers with a clean recent compliance history. That option matters because it can remove a penalty without requiring the same level of factual proof as a reasonable cause request, although filing compliance still matters.

The return usually must be filed before relief is considered.

A taxpayer asking for help without first fixing the missing return problem gives the IRS little reason to grant leniency.

What to Gather Before Requesting Penalty Relief

Build a file before you call or write the IRS.

A clear timeline, copies of each IRS notice, payment history, medical or disaster records, and a written explanation connecting the event to the late filing or late payment gives the request substance instead of excuses.

Frequently Asked Questions (FAQs)

What happens if you are late in filing your taxes?

If you owe taxes, the IRS can assess a failure-to-file penalty, a failure-to-pay penalty, and interest. Filing quickly usually stops the larger late-filing penalty from growing.

How much is the IRS tax penalty for late filing?

It is commonly 5% of unpaid tax for each month or partial month the return is late, up to 25%. If the return is more than 60 days late, a minimum late-filing penalty may apply.

What happens if you don’t file by April 15th?

You may face penalties if you have a balance due, but the exact due date can shift from April 15 because of weekends or holidays. File as soon as possible and use IRS payment options if you cannot pay in full.

What is the $600 rule?

The $600 rule usually refers to certain information reporting thresholds, often involving Form 1099 reporting. It is not the standard IRS penalty amount for filing a return late.

Filing late is fixable, but delay makes every part of the problem more expensive. File the return, pay what you can, respond to every IRS notice, and use available payment or relief options before penalties and interest grow into a much harder debt.

Categories: