Home  Blogs 2025 Tax Brackets: Federal Income Tax Rates, Filing Thresholds, and What Changed This Year

Blogs 2025 Tax Brackets: Federal Income Tax Rates, Filing Thresholds, and What Changed This Year

Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments Jan 13, 2025

Jan 13, 2025** updated 6-19-2026

The IRS bumped every income threshold in the 2025 tax brackets upward by roughly 2.8%.

That single change ripples through your 2025 tax filing from paycheck, your withholding, and your tax refund or balance due.

If you’re filing as a single taxpayer, a married couple, or a head of household, the federal income tax rates themselves haven’t moved. The seven rates still span 10% to 37%.

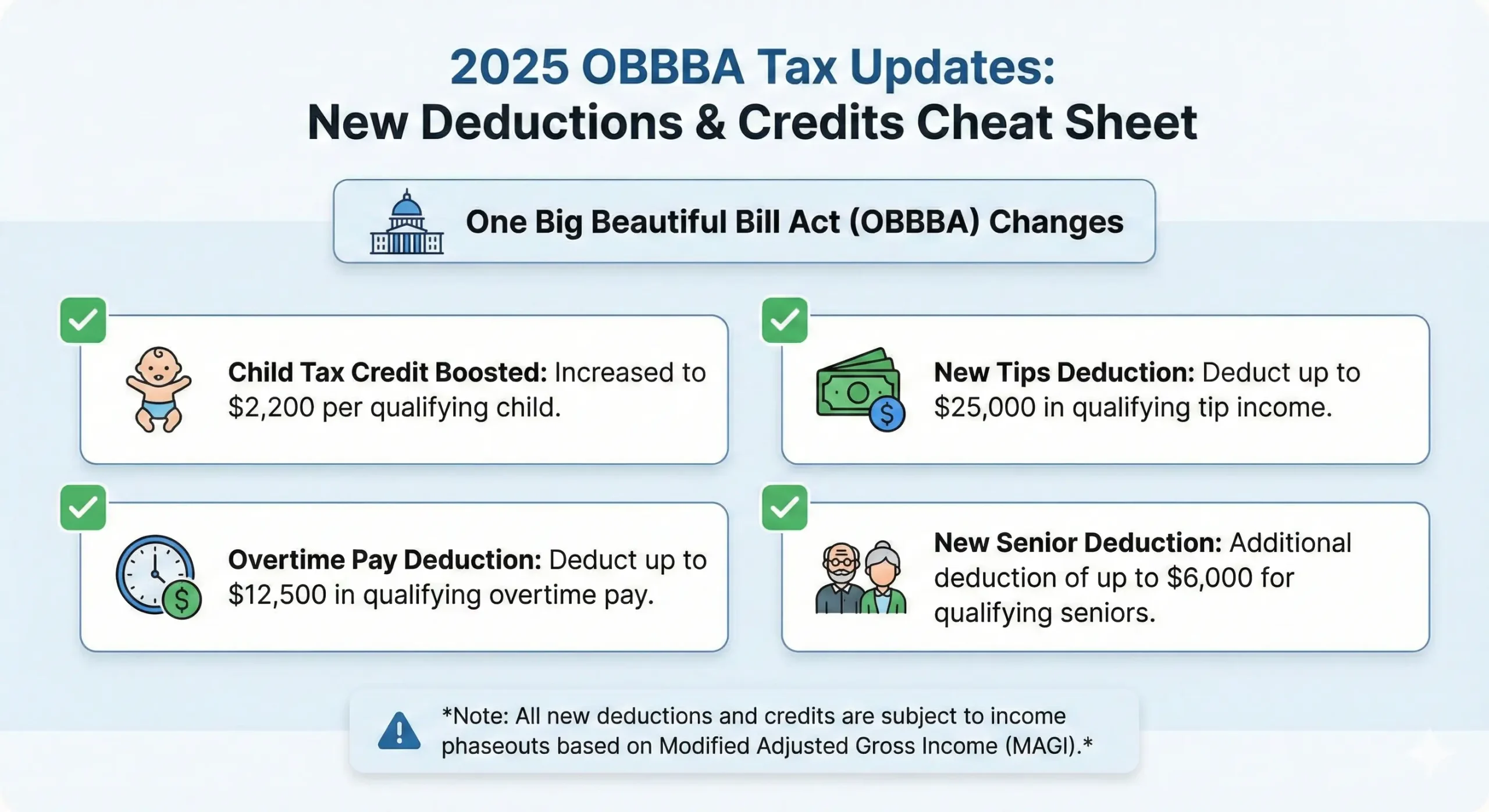

But the income ranges attached to each rate shifted enough to matter, and the One Big Beautiful Bill Act, signed into law on July 4, 2025, added several new tax provisions on top of those adjustments for your tax preparation this year.

Here’s what all of it means for your 2025 federal income tax return.

What Changed in the 2025 Federal Income Tax Brackets

Every year, the Internal Revenue Service recalibrates more than 60 tax provisions to keep pace with inflation.

These tax inflation adjustments exist to solve one specific problem: bracket creep. Without them, a cost-of-living raise that barely keeps up with grocery prices could shove you into a higher tax bracket, even though your purchasing power stayed flat.

For the 2025 calendar year, the IRS used the Chained Consumer Price Index to push income thresholds higher across all seven brackets. The tax code still contains the same federal income tax rates it has since 2018.

What changed are the dollar amounts where each rate kicks in.

The United States also saw significant tax reform through the One Big Beautiful Bill Act (OBBBA). That legislation made permanent most of the temporary tax law changes from the 2017 Tax Cuts and Jobs Act. It raised the standard deduction, boosted the Child Tax Credit, and introduced new deductions for tips and overtime pay.

So the 2025 tax year carries more moving parts than a typical inflation adjustment year.

The progressive tax system still works the same way it always has. Your total income gets divided into slices, and each slice is taxed at different rates. Nothing about that structure changed. The slices just got wider.

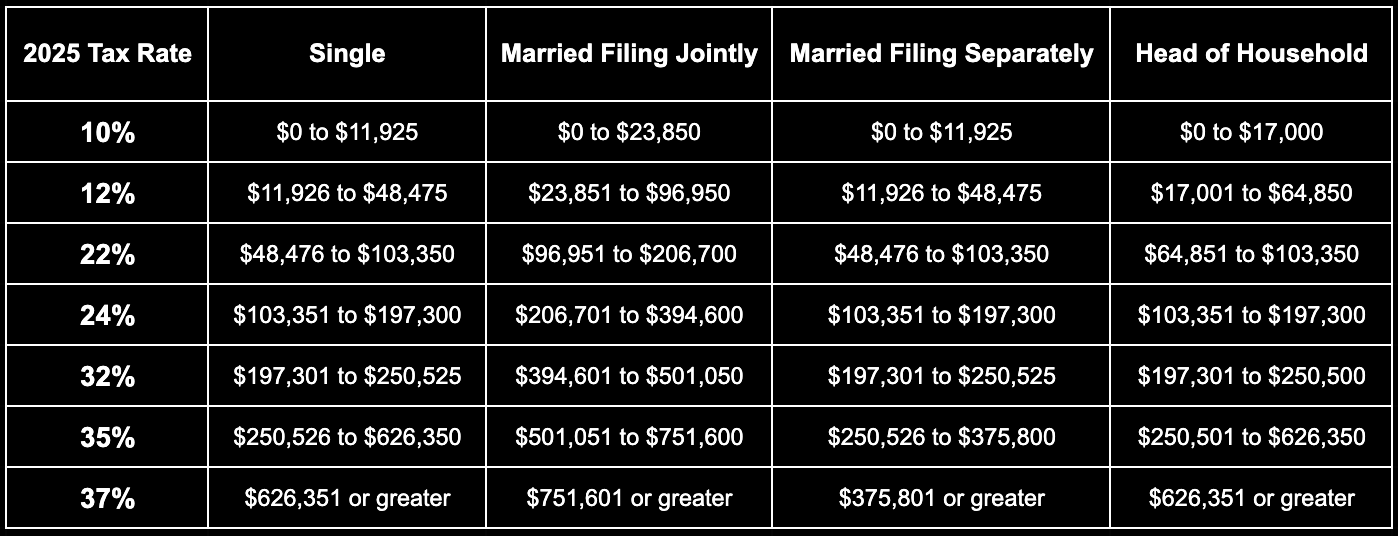

2025 Federal Income Tax Rates by Filing Status

Seven federal tax brackets apply to ordinary income in 2025. The federal tax rate you pay depends on where your taxable income lands within these income ranges.

Below are the bracket thresholds and federal income tax rates for each filing status.

Single Filers and Single Taxpayer Brackets

For single filers, the 2025 federal tax brackets break down like this:

- 10% on income from $0 to $11,925

- 12% from $11,926 to $48,475

- 22% from $48,476 to $103,350

- 24% from $103,351 to $197,300

- 32% from $197,301 to $250,525

- 35% from $250,526 to $626,350

- 37% on everything above $626,350

A single filer earning $60,000 in taxable income doesn’t pay 22% on the full amount. Only the portion above $48,475 gets taxed at that rate. The rest fills lower brackets first.

Married Filing Jointly and Surviving Spouse Brackets

Married couples filing jointly and qualifying surviving spouse filers use wider brackets that roughly double the single filer thresholds at the lower end:

- 10% on income from $0 to $23,850

- 12% from $23,851 to $96,950

- 22% from $96,951 to $206,700

- 24% from $206,701 to $394,600

- 32% from $394,601 to $501,050

- 35% from $501,051 to $751,600

- 37% on everything above $751,600

Notice that the doubling breaks down at higher income levels. The 37% bracket for married couples starts at $751,600, not $1,252,700 (which would be exactly double the single filer threshold). That gap is what people call the marriage penalty at the top end.

Heads of Households Bracket Thresholds

Head of household filers get bracket thresholds that fall between single and joint filers:

- 10% on income from $0 to $17,000

- 12% from $17,001 to $64,850

- 22% from $64,851 to $103,350

- 24% from $103,351 to $197,300

- 32% from $197,301 to $250,500

- 35% from $250,501 to $626,350

- 37% on everything above $626,350

To qualify, head of household filers must be unmarried, pay more than half their household costs, and have a qualifying dependent. Many eligible filers overlook this status, even though it offers lower bracket thresholds than filing as single.

Married Filing Separately

A married couple filing separate returns uses tax bracket thresholds that mirror the single filer brackets in most cases. Some married couples choose this path to keep their tax situations distinct or to protect one spouse from the other’s tax liabilities. But filing separately often means losing access to certain credits and tax breaks, so weigh your filing options carefully.

How Tax Brackets Actually Work (The Mistake Most Filers Make)

This is the most misunderstood concept in the federal income tax system.

Millions of filers believe that earning one extra dollar into a higher tax bracket means their entire paycheck gets taxed at the higher rate.

That’s wrong.

Here’s how brackets work in practice. Say you’re a single filer with $55,000 in taxable income for 2025. The IRS doesn’t multiply $55,000 by 22%.

Instead, your income fills each bracket sequentially:

First, $11,925 gets taxed at 10%, producing $1,192.50 in tax. The next $36,550 (the slice from $11,926 to $48,475) gets taxed at 12%, adding $4,386. Then only the remaining $6,525 above $48,475 hits the 22% rate, contributing $1,435.50.

Your total federal tax bill on $55,000 comes to $7,014. That’s an effective tax rate of about 12.75%, far below the 22% bracket you technically sit in. This gap exists because marginal tax rates only apply to income within each bracket, not to every dollar you earn.

So when your income increases and pushes you into a higher tax bracket, only the dollars above the threshold get taxed at the higher rate. The amount of tax on your lower income stays exactly the same.

Why does this matter?

Because fear of a higher rate stops some people from pursuing raises, bonuses, or overtime pay. Earning more always leaves you with more after taxes. Always.

2025 Standard Deduction and Key Tax Provisions

The standard deduction reduces your taxable income before the federal tax rate schedule even applies. For 2025, the OBBBA boosted these amounts beyond the normal inflation adjustment:

- Single filers: $15,750

- Married Filing Jointly: $31,500

- Heads of Households: $23,625

Filers aged 65 and older can claim an additional standard deduction of $2,000 (single) or $1,600 (joint). The OBBBA also created a separate senior deduction of up to $6,000 for qualifying taxpayers, with phaseout thresholds starting at $75,000 for single filers and $150,000 for joint filers based on modified adjusted gross income.

If your itemized deductions exceed these standard amounts, you’ll want to itemize instead. Common itemized deductions include state income tax and local taxes (capped under SALT rules), medical expenses exceeding 7.5% of AGI, and mortgage interest. Keep in mind that payroll tax is separate from income tax and doesn’t factor into your bracket calculation.

The Child Tax Credit rose to $2,200 per qualifying child under the OBBBA, up from $2,000.

The refundable portion remains at $1,700. Phaseout thresholds sit at $200,000 for single filers and $400,000 for joint filers. The Earned Income Tax Credit for 2025 tops out at $8,046 for filers with three or more qualifying children, with income limits that vary by filing status and number of dependents.

The Alternative Minimum Tax still applies as a parallel calculation. For 2025, the AMT exemption amount is $88,100 for single filers and $137,000 for married couples filing jointly. If your income exceeds those levels, you may need to calculate your tax under both systems and pay whichever produces the larger bill.

Long-Term Capital Gains Tax Rates for 2025

Profits from selling investments held longer than one year face long-term capital gains tax rates that sit well below ordinary income rates.

Three capital gains tax rates apply in 2025:

The 0% rate covers taxable income up to $48,350 for single filers and $96,700 for married couples filing jointly.

The 15% rate applies to income levels between those thresholds and $533,400 (single) or $600,050 (joint).

Everything above those ceilings gets taxed at 20%.

These capital gains tax brackets are separate from the regular federal income tax brackets. A single filer with $45,000 in wages and $10,000 in long-term capital gains would first apply their ordinary income to the regular brackets, then layer the capital gains on top using the capital gains rate schedule.

High earners may also owe an additional 3.8% Net Investment Income Tax.

Short-term gains on assets held one year or less don’t get this preferential treatment. They’re taxed as ordinary income at your regular federal tax rate.

Strategies to Lower Your 2025 Tax Bill

Knowing your bracket is useful. Doing something about it is better.

Retirement accounts offer the most accessible tax deductions for most filers.

The maximum amount you can contribute to a 401(k) or similar retirement plan in 2025 is $23,500, with a $7,500 catch-up for filers aged 50 and older. Those retirement contributions come straight off your taxable income. Traditional IRAs allow up to $7,000 in contributions ($8,000 if you’re 50 or older), though income limits may restrict deductibility if you’re covered by a workplace retirement plan.

A Roth IRA doesn’t reduce your current tax bill, but qualified withdrawals in retirement come out tax-free, making it a strong financial planning tool for retirement savings.

Beyond retirement accounts, other tax-advantaged vehicles help too.

A health savings account lets you stash up to $4,300 (individual) or $8,550 (family) in 2025, and contributions reduce your taxable income. A Flexible Spending Account through your employer works similarly for healthcare or dependent care expenses, though the contribution limits are lower and unused funds may expire.

The OBBBA introduced new tax breaks for 2025. Qualifying workers can deduct up to $25,000 in tips and up to $12,500 in overtime pay from their taxable income, subject to income phaseouts. Car loan interest on qualifying vehicle purchases also became deductible under the new law. These tax provisions phase out for filers with modified adjusted gross income above $150,000 ($300,000 for joint filers).

Tax planning doesn’t have to be complicated.

Even straightforward moves, like timing a large charitable donation or accelerating a deductible expense, can shift income between brackets and produce real tax savings and tax benefits.

Filing Your 2025 Tax Return: Where to Start

Tax forms and instructions for the 2025 tax year are available on IRS.gov.

File by April 15, 2026, or request an automatic extension to October 15. You’ll report your income, apply your deductions, and calculate your liability using the Tax Rate Schedule for your filing status.

Complex returns benefit from professional help. If your tax situation involves multiple income sources, investment gains, or self-employment income, a tax professional can spot deductions you’d otherwise miss. Even a one-time session with a tax preparer or tax advisor pays for itself when the savings outweigh the fee. For ongoing planning, a tax pro or tax expert who knows your full picture can keep your income tax return optimized year after year. This article does not constitute tax advice or legal advice. Every filer’s specific situation differs, and a qualified third party can review yours.

For straightforward W-2 returns, free filing options exist through the IRS Free File program or commercial tax software. Don’t leave money on the table. Claiming every deduction and credit you’re entitled to is the simplest path to a larger tax refund.

Looking for more tax help and tax resources?

The IRS Taxpayer Advocate Service handles disputes. Tax Tips published by the IRS cover seasonal updates. And your state’s department of revenue can clarify how state income tax stacks on top of your federal brackets.

Your Next Move for 2025

The 2025 federal income tax brackets give you a framework.

The deductions, credits, and retirement vehicles give you levers to pull.

What matters now is applying both to your own numbers. Pull up last year’s return, compare it to this year’s income, and run the math on an extra retirement contribution or a deduction you haven’t claimed before.

The tax code rewards people who plan. And the sooner you understand where your income sits within these brackets, the sooner you stop overpaying.

Reach out to your dedicated PriorTax professional today to guide you from start to finish.

Categories: