Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments Mar 31, 2026

Mar 31, 2026*updated 6-19-2026

Key Takeaways

- File prior-year returns for any unfiled year, but prioritize years still inside the three-year refund deadline first

- Choose the six-year compliance path when IRS notices have not arrived and no collection activity is active

- File before the IRS finalizes a Substitute for Return to preserve deductions, credits, and accurate numbers

- Use an IRS account transcript and wage and income transcript to confirm every missing year before filing

- File all back taxes first even without full payment — installment agreements handle the tax debt afterward

- A tax professional ensures each prior-year return claims every deduction and credit you qualify for

- PriorTax specializes in prior-year returns, filing accurately and affordably with transparent pricing and no hidden fees

Missing a tax return filing can sit in the back of your mind for years, especially if you are not sure whether the IRS still expects it.

When people ask about how many years to file back taxes, they usually mean one of three things: how far back they can submit a return, how long they have to claim a refund, and how many years the Internal Revenue Service typically wants to restore tax compliance.

The short answer to what happens if you file taxes late is this: you can generally file old tax returns for any unfiled year, even if they are very late.

A practical IRS compliance standard often focuses on the last six years of past due tax returns, but that is not the same as a hard legal limit.

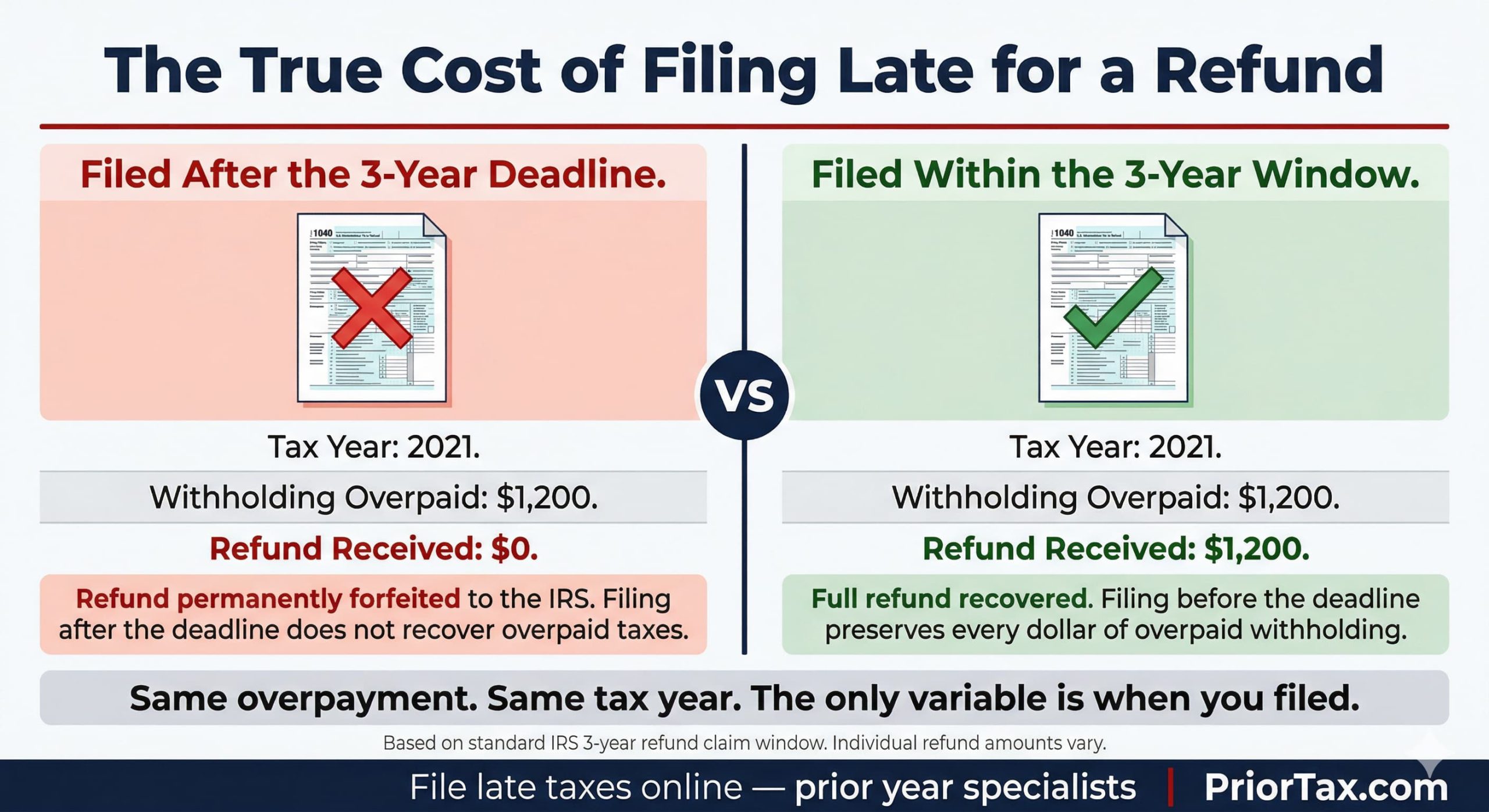

Refunds follow a tighter rule. If you are owed money, you usually must file within three years of the original return due date to claim a refund, recover withholding, or get credit for estimated taxes.

One more point matters a lot. If a required original return was never filed, the normal statute of limitations on assessment usually does not begin, which means that tax year can stay open indefinitely.

Answer the Core Question Up Front

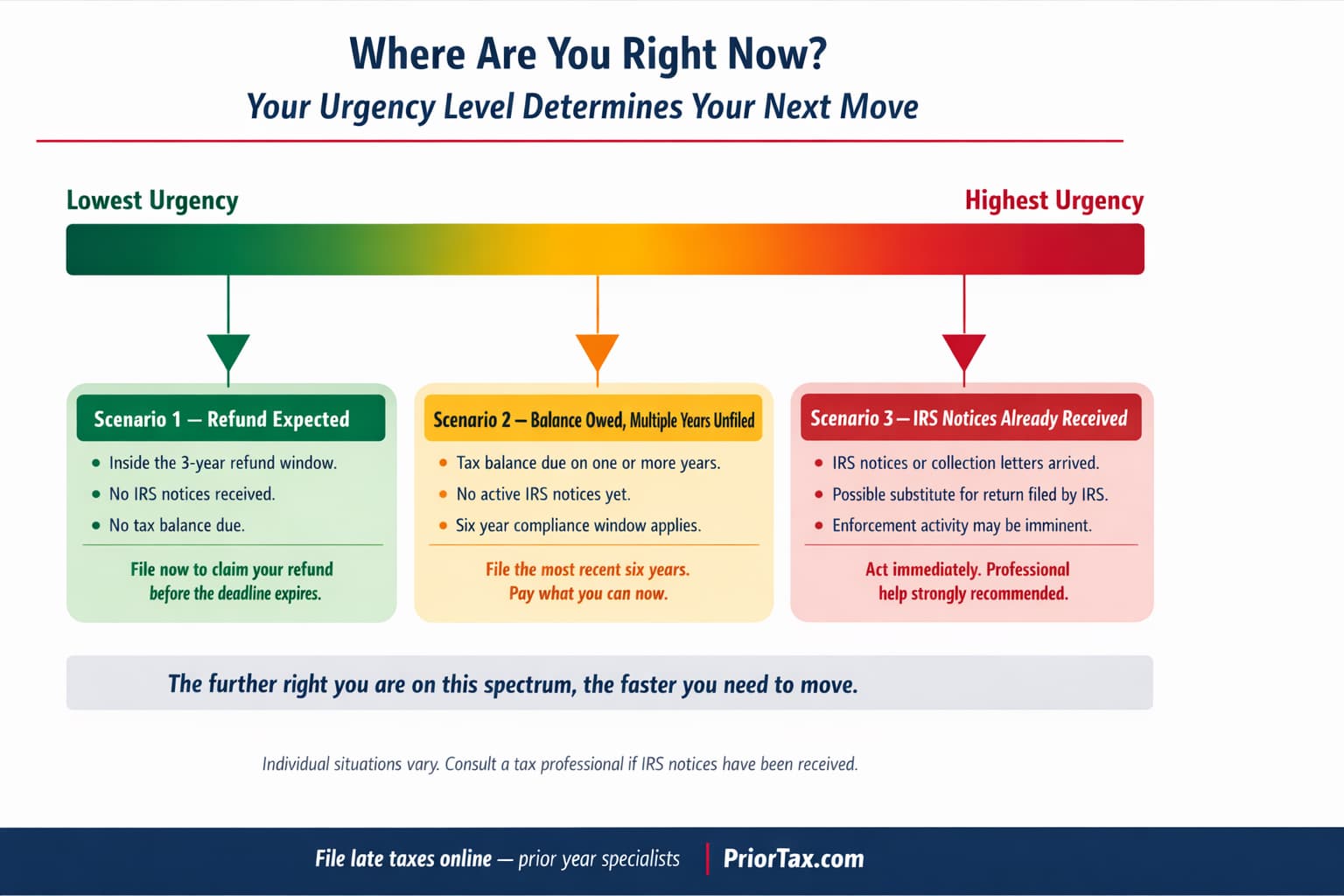

Taxpayers can usually submit prior-year returns even when they missed the tax deadline or even several years late. Old back taxes do not become unfileable just because the filing deadline passed.

That said, the exact number of years depends on your goal. Someone trying to get back into federal tax compliance faces a different timeline than someone trying to claim a refund.

For many delinquent returns, the IRS commonly expects the last six years to be filed to bring an account into good standing. Tax professionals often refer to this as the six-year rule, though it is really a compliance guideline rather than a universal cap.

Refund claims work differently. A taxpayer who overpaid through withholding or estimated taxes generally has only three years from the return due date to file and recover that money.

Miss that refund deadline and the money may be lost, even if the tax return shows no tax debt at all. That catches many people by surprise.

Unfiled returns also create a separate risk. When no required return was filed, the IRS can assess tax later because the normal assessment period has not started.

So if your question is whether you can still file previous year taxes from long ago, the answer is usually yes. If your question is whether you can still get money back, the answer may be no once the three-year rule has expired.

The Short Answer Most Readers Need

You can usually file back taxes for old years, even if those returns are very late. Many non-filers are asked to cover the most recent six years first.

Why the Exact Number of Years Depends on the Goal

Refund rights, tax compliance, and collection risk each follow different rules. A refund claim may expire quickly, while non-filing can stay open much longer.

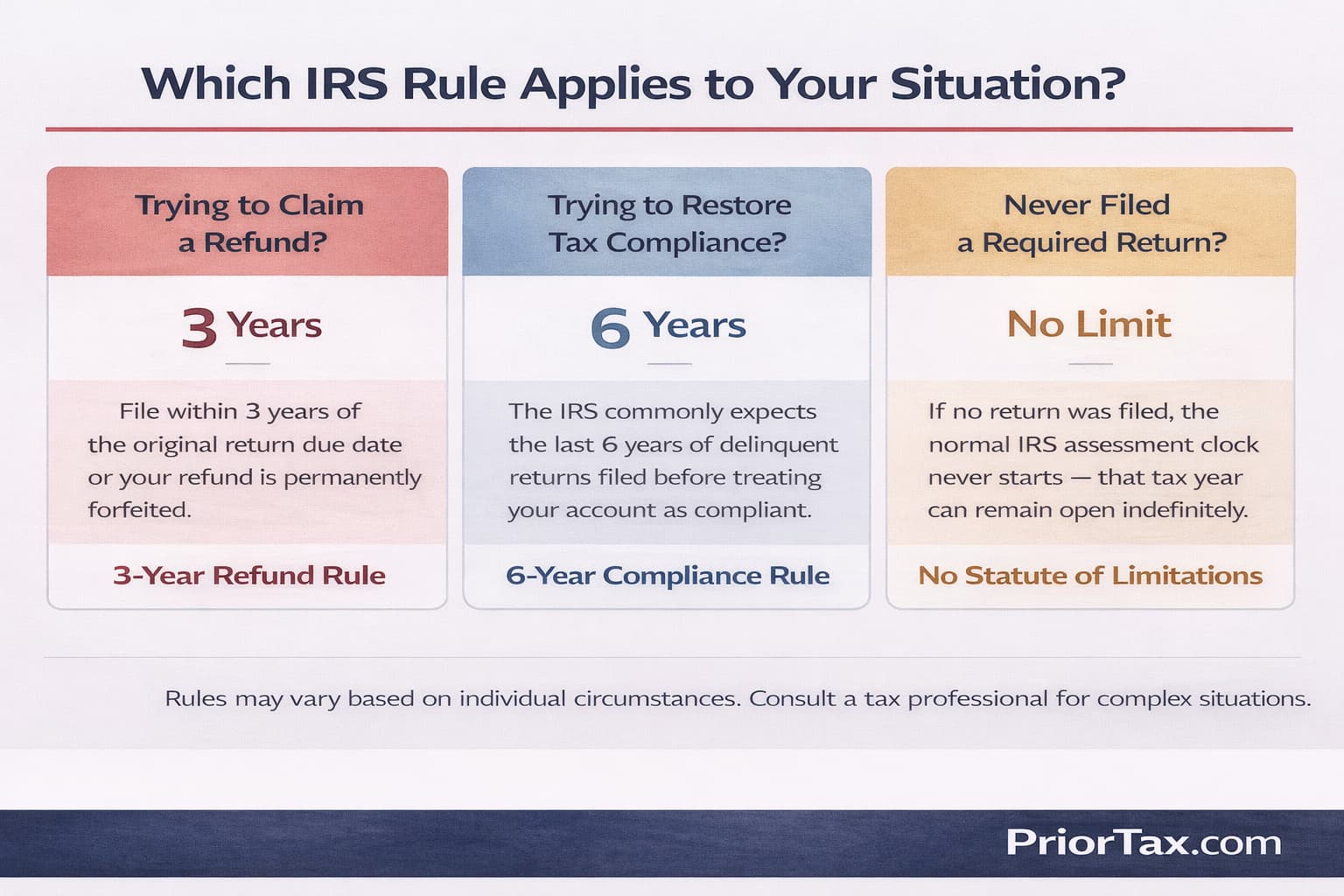

Understand the Main IRS Time Limits

Most confusion comes from mixing up three separate deadlines. The refund window, the six-year compliance benchmark, and the statute of limitations for assessment do not mean the same thing.

The three-year rule matters when the IRS owes you money. The six-year rule often comes up when you need to fix non-filing and get back into good standing.

Another rule is less forgiving. If you never filed a required tax return, the normal clock that limits IRS assessment usually does not start running.

That is why old unfiled returns can still create problems many years later. Waiting does not usually erase the issue.

The Three-Year Refund Rule

If a taxpayer is due a refund, the return generally must be filed within the three year rule of the filing deadline to claim a refund. That includes money tied to withholding and many estimated taxes.

After that, the refund claim usually expires. Even if the IRS would agree that you overpaid, the law may block the payment.

The two-year rule can also matter in some refund claim situations tied to payments made later. In practice, most late filers asking about old refunds focus first on the three-year rule.

The Six-Year Compliance Rule

The six-year rule usually means the IRS often wants the last six years of delinquent returns filed before treating a taxpayer as compliant. This standard appears often in practice and in IRS-facing guidance used by tax professionals.

Still, six years is not a firm cutoff on how far back a prior-year return can be filed. Older years may still matter if there is a large tax bill, business returns, or active IRS enforcement.

No Statute of Limitations on Unfiled Returns

A filed return usually starts the normal assessment period. No filed return means that protection generally never begins.

That leaves the year open for the IRS to assess tax later. Non-filing can remain a live issue indefinitely even after factoring in IRS statute of limitations.

What Happens If You Wait Too Long

Delay gets expensive fast. Penalties and interest keep building, and some rights disappear while you wait.

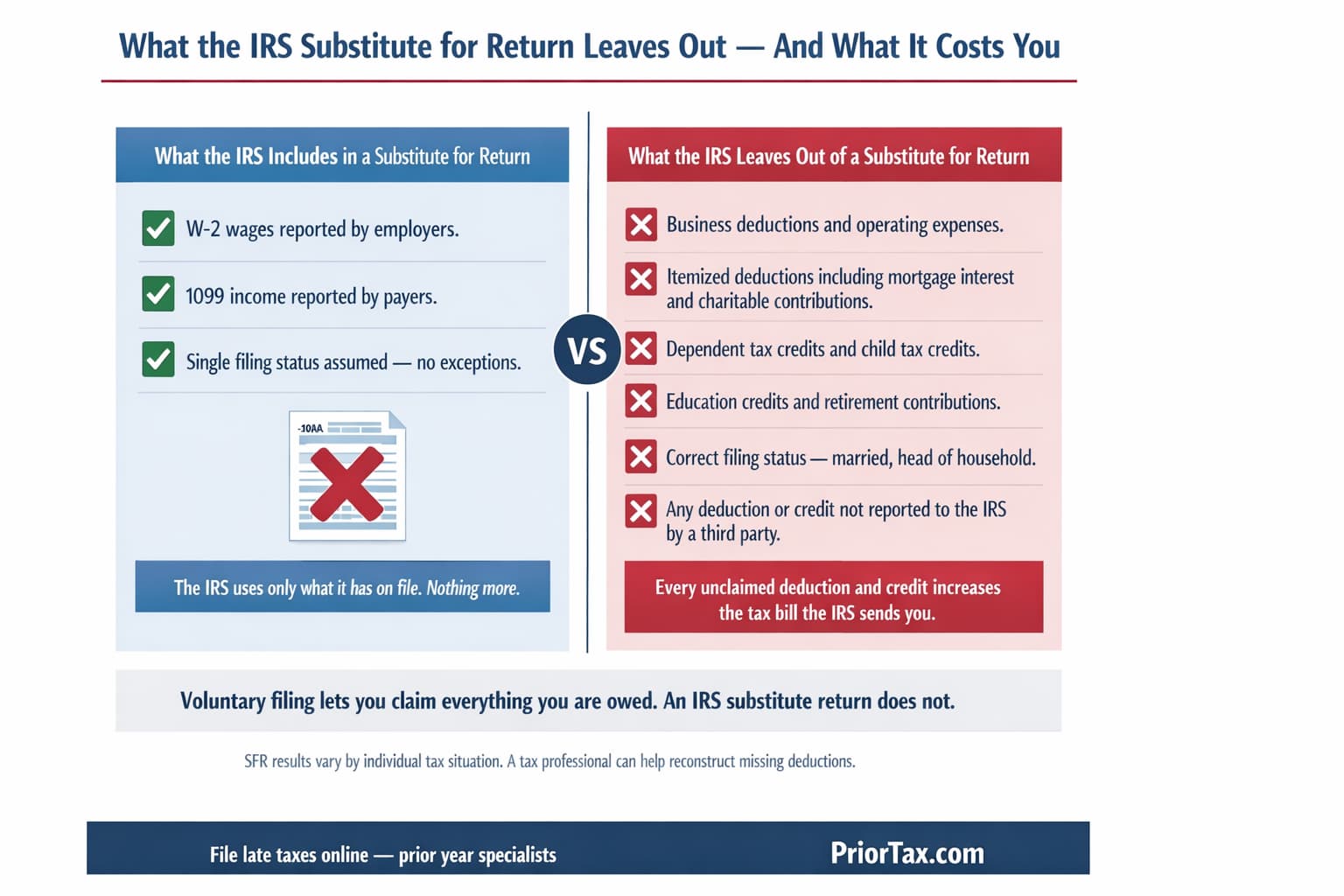

Another problem shows up when the IRS has income records but no tax return from you. The agency can prepare a substitute for return, often called an SFR, based on limited information.

That result is rarely favorable. A substitute for return may ignore deductions, credits, and filing positions that could reduce the tax bill.

Voluntary late filing usually puts you in a better position than waiting for enforcement. Once IRS notices start piling up, your options can narrow.

Penalties and Interest Keep Growing

The failure-to-file penalty can rise quickly when a return is late and tax is due. The failure-to-pay penalty and interest usually continue until the balance is paid.

Those charges can turn a manageable tax debt into a much larger problem. Late filing often costs more than people expect.

You May Lose Refunds and Credits

Late filing does not only hurt taxpayers who owe money. A missed refund deadline can wipe out a refund, withholding recovery, or some credits.

That matters for people who assume no filing means no downside. Sometimes the taxpayer was due money all along.

The IRS May File for You

An SFR (substitute for return) is the IRS version of your return, not your best-case return. It often includes income from W-2 and 1099 records but leaves out deductions and credits you could have claimed.

That can create a higher tax bill than a properly prepared original return. Once that happens, fixing the year can become more urgent.

How to Figure Out Which Years You Need to File

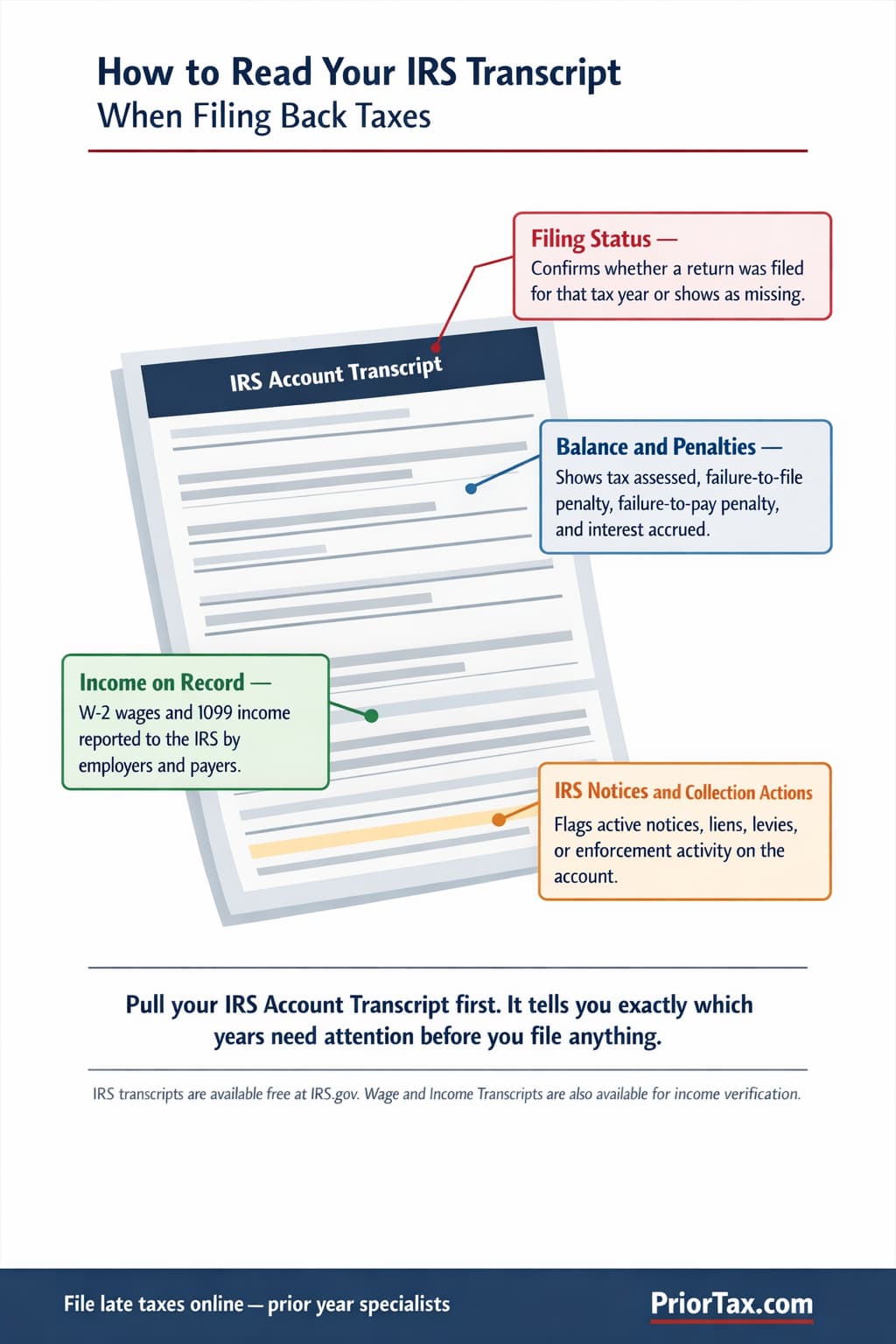

Start by identifying every missing year instead of guessing. Many people remember being late, but not whether a return was actually filed.

Your IRS account can help. An account transcript may show filing status, balances, and collection activity, while a wage and income transcript can list W-2, 1099, and other information returns reported under your Social Security number.

This review helps you separate years that matter for compliance from years that may still produce a refund. The distinction saves time.

Review Your IRS Account and Transcripts

Check your IRS transcript records first. The account transcript and wage and income transcript are often the fastest way to confirm unfiled returns and reconstruct missing income data.

An IRS transcript can be especially useful if your records are incomplete. It gives you a starting point for preparing a prior-year return.

Prioritize the Most Important Years First

Look first at years still inside the refund deadline. If a refund may be available, file those returns before the three-year window closes.

After that, focus on the most recent six years to align with common IRS tax compliance expectations. That order often makes practical sense.

Check for Special Situations

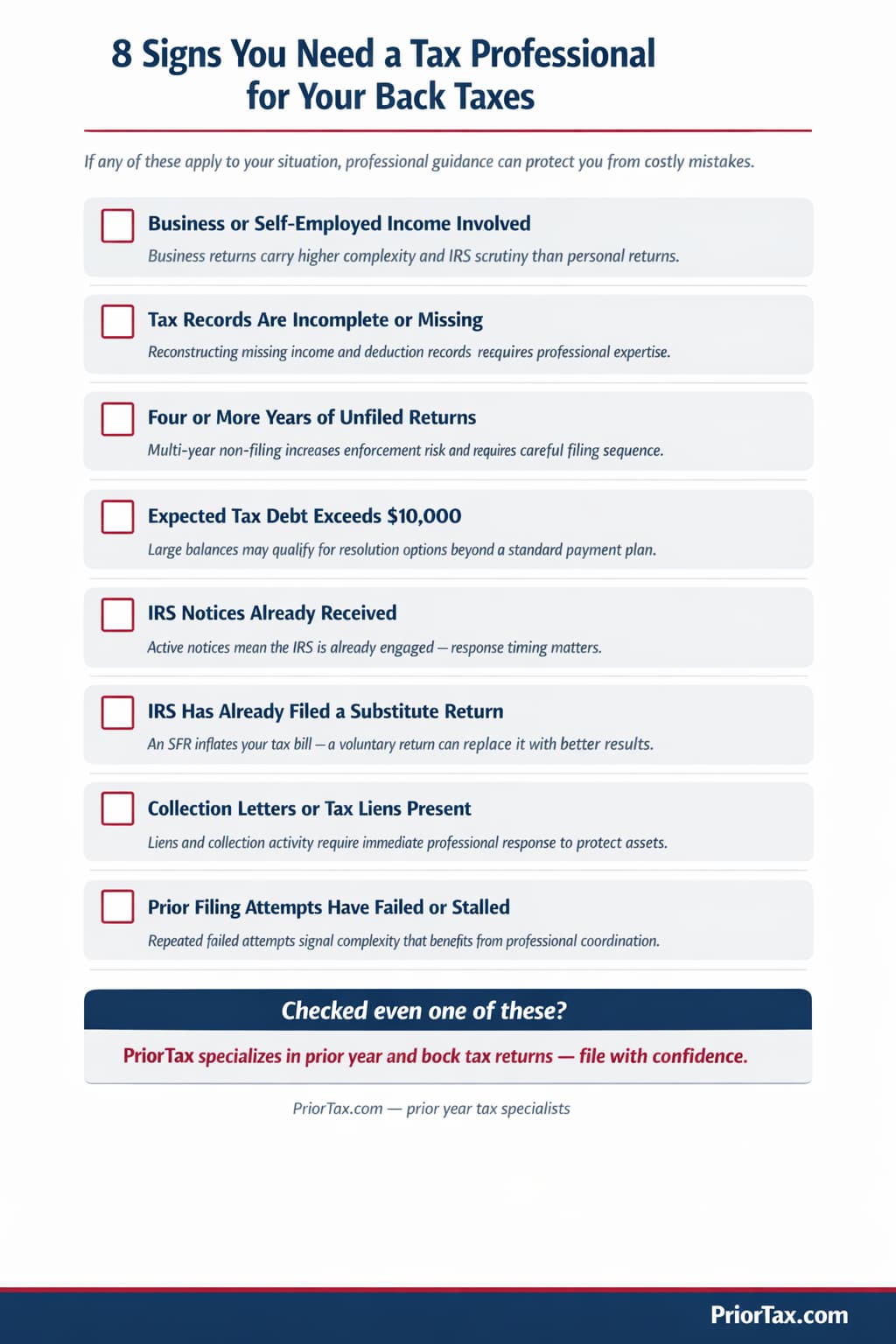

Business returns, self-employed income, and years with large balances due deserve closer attention. IRS notices, audits, or collection activity can also change the filing strategy.

Some cases need more than simple catch-up filing. Tax resolution planning may be necessary if exposure is high.

Step-by-Step Process for Filing Back Taxes

A clear process keeps old returns from becoming a bigger mess. You do not need to solve every issue at once, but you do need the right order.

File the correct form for each year. A 2022 return must be prepared under 2022 rules, and the same goes for every other prior-year return.

If you cannot pay in full, file anyway. Payment options can be handled after the returns are submitted.

Gather Prior-Year Tax Documents

Collect W-2s, 1099s, prior IRS notices, and records for deductions. Pull bank statements, business logs, and expense records if you are self-employed.

Missing documents do not end the process. Use transcripts and careful reconstruction where needed.

Prepare Each Return Using That Year’s Rules

Tax law changes from year to year. Rates, credits, deductions, and prior-year forms must match the specific tax year being filed.

That is why current-year software cannot always fix previous year taxes correctly. Prior-year software or a tax professional can reduce errors.

File First, Then Resolve the Balance

Filing late and paying late are separate problems. Filing can reduce failure-to-file penalty exposure even if the tax debt remains unpaid.

After filing, review payment plan options such as an installment agreement. The IRS may also offer other tax resolution paths depending on the balance and your finances.

Examples That Clarify Common Scenarios

Rules make more sense when you attach them to real dates. A few simple examples show why the answer changes depending on whether the issue is a refund or non-filing.

The same taxpayer could have one year that is still worth filing for a refund and another year that is only about compliance. Timing matters.

Example: A Taxpayer Owed a Refund

Suppose a taxpayer was due a refund for tax year 2022, and that return was due in 2023. That person generally has about three years from the original due date to claim a refund.

If the return is filed after that refund deadline, the refund may be gone permanently. The overpayment does not always come back just because it can be proven.

Example: A Taxpayer Has Not Filed for Eight Years

Assume someone has eight years of unfiled returns and no active enforcement yet. The IRS may focus first on the most recent six years to restore good standing.

Older years can still matter, though. Large unpaid balances, business returns, or strong IRS records of income may lead the agency to look beyond six years.

Example: The IRS Already Sent Notices

Now assume IRS notices have already arrived for missing returns or collection. That taxpayer should move quickly because the case may be closer to enforcement.

Filing before the IRS finalizes an SFR often leads to a better result. Professional help may be useful at that stage.

Common Mistakes to Avoid With Unfiled Returns

People usually make the same few errors when dealing with back taxes. Most of them come from waiting too long or using the wrong assumptions.

A small mistake can delay processing. A bigger one can increase the tax bill.

Assuming Old Tax Debt Goes Away on Its Own

Unfiled returns do not usually age out the way people hope. If no required return was filed, the year may remain open with no clear end point.

Silence from the IRS does not prove the issue is resolved. Non-filing can surface later through matching programs or enforcement action.

Using the Wrong Year’s Forms

Each delinquent return needs the forms and instructions for that specific year. Current forms can produce wrong numbers because tax brackets, deductions, and credits change.

Use prior-year forms and year-specific rules. That is basic, but it matters.

Waiting to File Until You Can Pay in Full

Many taxpayers delay because they fear the tax bill. That usually makes things worse.

Filing and payment are separate. File first to limit the failure-to-file penalty, then work on a payment plan or installment agreement.

When to Handle It Yourself and When to Get Help

Some late returns are straightforward. Others carry enough risk that DIY filing is not the smart move.

The difference usually comes down to complexity, missing records, and how much IRS involvement already exists. A simple wage-only case is very different from a self-employed taxpayer with several years of unfiled returns.

Situations Suitable for DIY Filing

A few missing personal returns with basic W-2 income may be manageable on your own. IRS transcript data and prior-year software can help you rebuild the file.

This approach works best when there are no business returns, no major deductions issues, and no serious IRS notices. Clean facts make DIY more realistic.

When Professional Help Is Worth It

Get a tax professional or involved if business returns are missing, records are incomplete, or tax attorney if the expected tax debt is large. Help is also wise when collection staff, audits, or repeated IRS notices are already in play.

A tax professional can coordinate the filing order, respond to notices, and structure tax resolution options. That can matter a lot when exposure is high.

Action List For Filers Ready to Act

You can usually file old tax returns for any unfiled years (tax years 2024, 2023, 2022) even if they are years late. The bigger question is what you are trying to accomplish.

If you want money back, the three-year rule usually controls your refund claim. If you want to restore federal tax compliance, the six-year rule is a common benchmark the IRS uses in practice.

No filed return usually means no normal statute of limitations on assessment. That is why ignoring past years tax returns rarely solves anything.

Start by identifying missing years through your IRS account transcript and wage and income transcript. Gather records, prepare each original return using that year’s rules, file as soon as possible, and then address payment through a payment plan or other resolution if needed.

Common Questions (FAQs)

What is the IRS 7 year rule?

There is no single universal IRS seven-year rule for filing back taxes. People often confuse several deadlines, but the most relevant are the three-year refund deadline and the common six-year compliance benchmark.

What happens if you don’t file taxes for 7 years?

The IRS may require multiple delinquent returns, add penalties and interest, and prepare a substitute for return. Many cases focus first on the most recent six years, but older years can still matter.

What is the IRS six year rule?

The IRS six year rule usually refers to the common expectation that many non-filers submit the last six years of returns to regain compliance. It is a practical guideline, not a hard legal filing limit.

At what point will the IRS come after you?

There is no exact trigger for every taxpayer. IRS enforcement depends on reported income, missing returns, balances due, ignored IRS notices, and whether collection activity has already started.

Categories: