Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments Mar 17, 2026

Mar 17, 2026*updated 6-19-2026

Key Takeaways

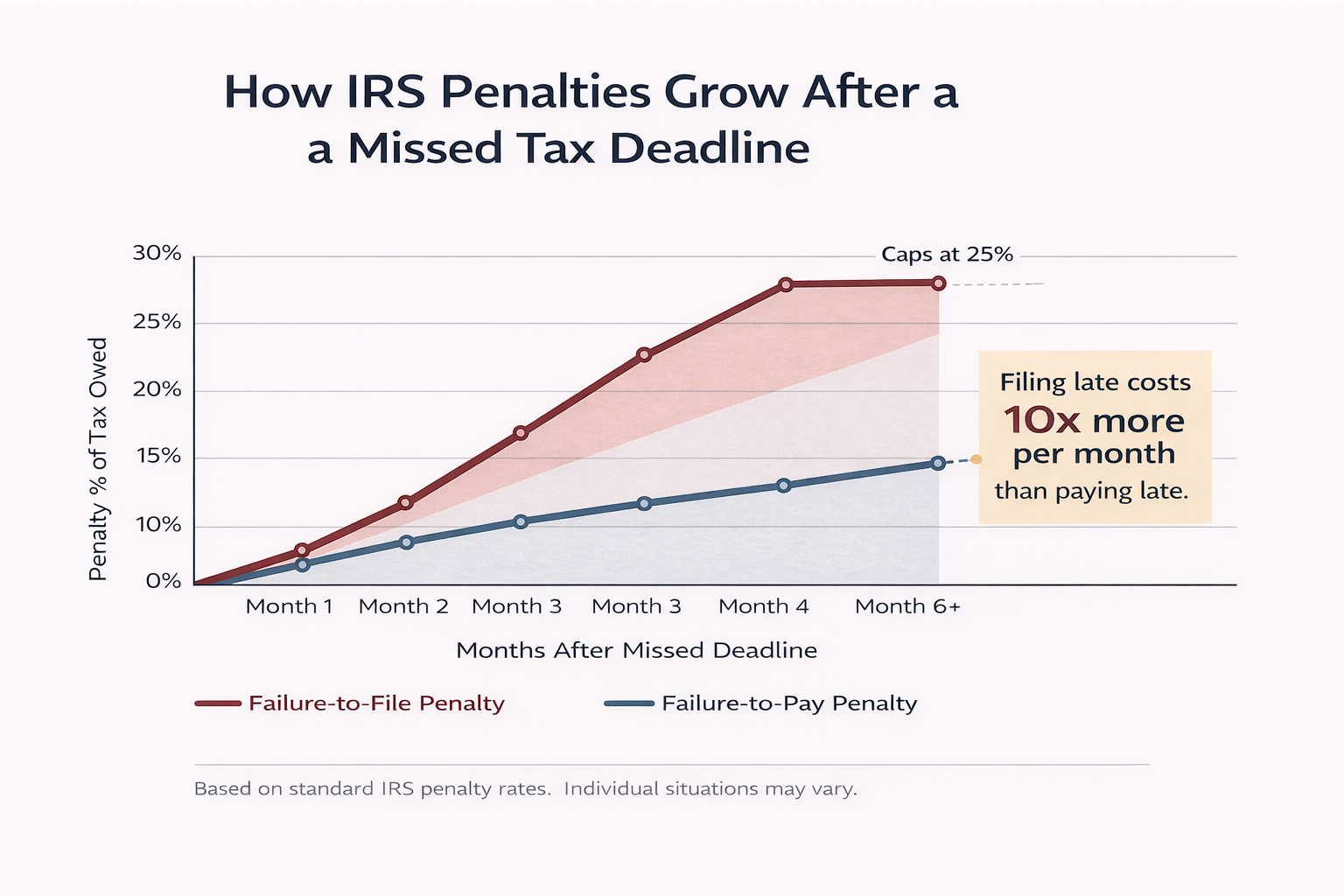

- The failure-to-file penalty charges 5% of unpaid taxes monthly, capped at 25% of the total

- IRS assesses a separate failure-to-pay penalty of 0.5% monthly on any outstanding balance, capped at 25% of the total

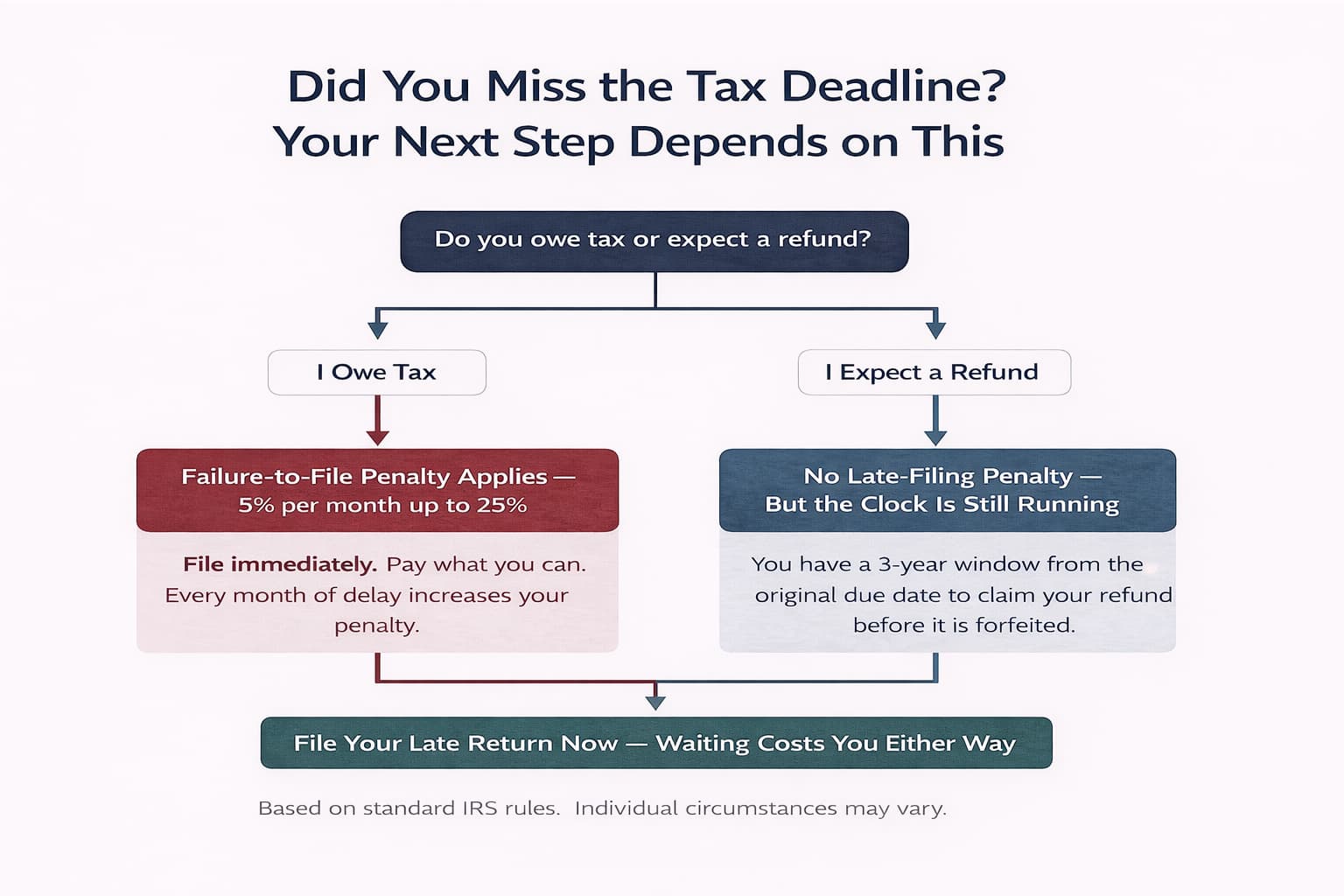

- Refunds carry no late-filing penalty, but the three-year refund window still closes eventually

- Interest accrual continues on unpaid taxes even after an installment agreement is approved

- Refund claim deadline runs three years from the original tax filing deadline

- Late returns for prior years can be e-filed online at PriorTax.com — no tax professional required

Tax day comes fast, and plenty of people realize too late that April 15 has passed. If you are dealing with a missed tax deadline, the next move matters more than the mistake itself.

The IRS has rules for late filing, late payment, extensions, refunds, and relief requests, and each one affects what you owe or recover.

This guide explains what happens after the tax filing deadline, what to do right away, and how to file your back taxes online before the problem grows.

Understand What Happens After a Missed Tax Deadline

Missing the tax return deadline does not trigger one single consequence – to understand the full penalty picture, see what happens if you file taxes late.

The IRS treats filing late and paying late as separate issues, which means a federal tax return can be filed after the due date and still leave a tax balance due that keeps growing.

That distinction matters.

A late return can trigger a failure-to-file penalty when tax is owed. An unpaid balance can trigger a failure-to-pay penalty and interest charges, even if the paperwork is eventually submitted.

Time makes both problems more expensive. Penalties and interest usually increase while unpaid taxes remain on your account, and interest accrual continues until the tax owed is fully paid.

People expecting a refund often face a different outcome.

If the IRS owes you money, a late-filing penalty usually does not apply, but delayed refunds mean you wait longer to get funds that may already be yours.

IRS deadlines still matter even when no penalty applies. A refund claim deadline exists, and the three-year refund window generally starts from the original due date of the return.

Late Filing vs. Late Payment

The failure-to-file penalty is the charge for not submitting your tax return on time when you owe tax. It is usually more severe than the failure-to-pay penalty, which is why filing quickly often saves money even if you cannot pay in full.

The failure-to-pay penalty applies when tax remains unpaid after the due date. That charge focuses on the unpaid amount, while filing consequences relate to the missing or late return itself.

When a Refund Changes the Outcome

A refund changes the urgency from a penalty standpoint because the IRS generally does not assess a late-filing penalty when no tax is owed. Still, filing late can delay access to that refund and create recordkeeping issues later.

The refund claim deadline is not open forever. Most taxpayers have a three-year refund window to file and claim a refund before it is forfeited.

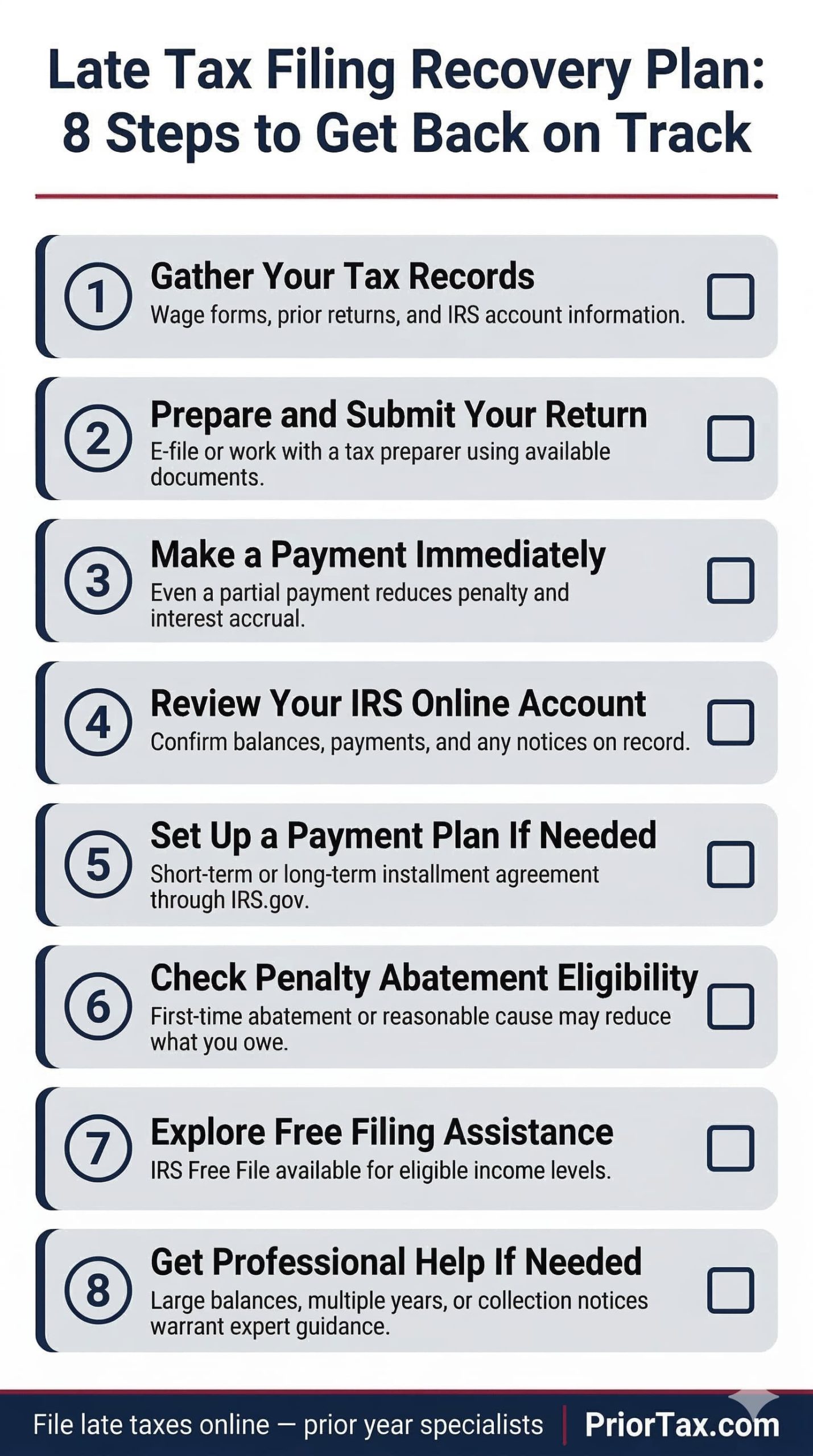

Take These Immediate Steps If You Missed the Due Date

Start with the return.

File as soon as possible, even if your records are incomplete and even if you cannot pay the full tax balance due.

Waiting for perfect paperwork often costs more than filing a good-faith return now and correcting it later if needed. If enough tax records are available to prepare an accurate income tax return, submit it.

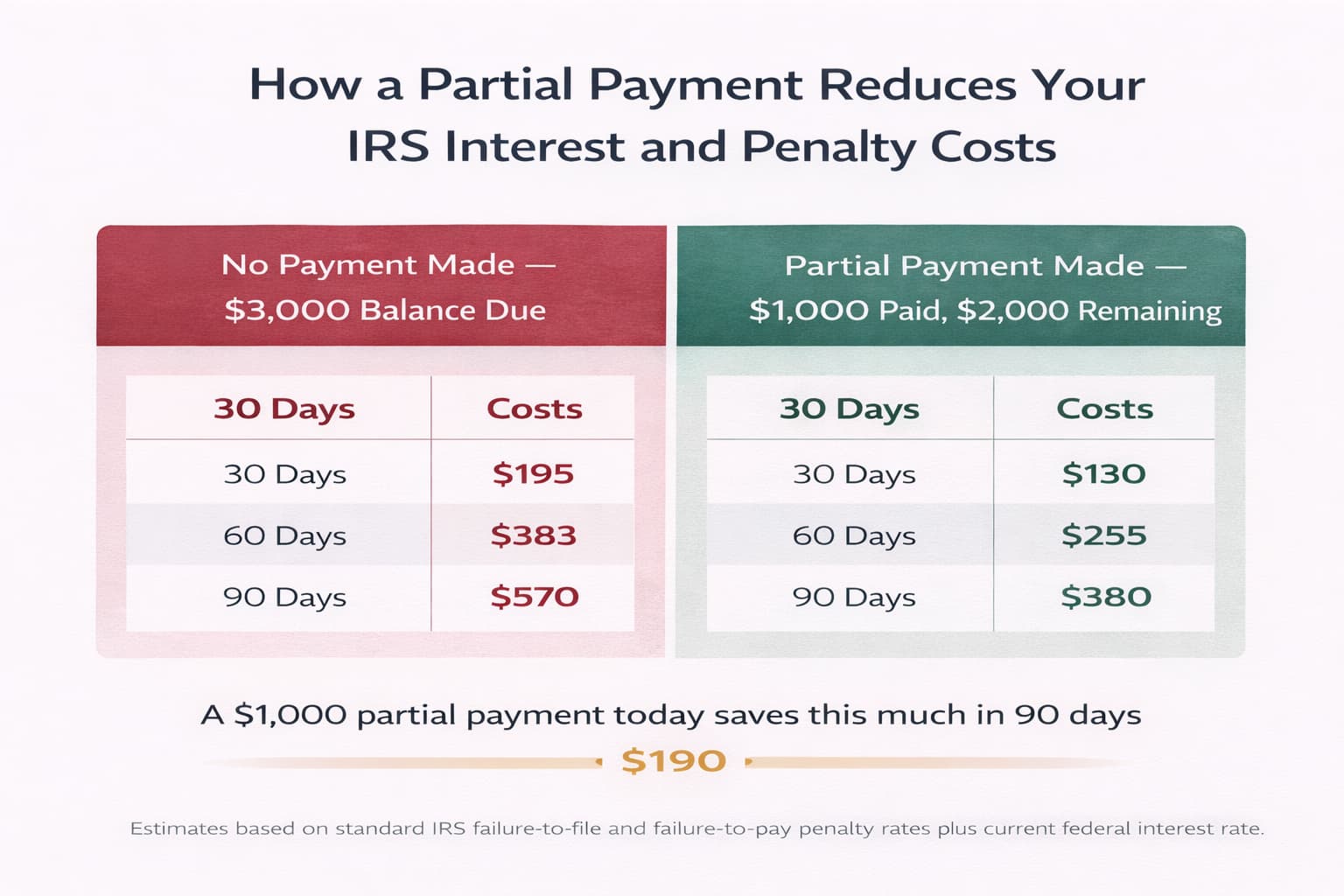

Then estimate what you owe and pay now. A partial payment reduces the amount subject to interest charges and may cut down the late payment cost.

Use IRS.gov tools when possible. The IRS online account can help you review balances, payments, and notices, and gives you a clearer picture of what happened after the tax filing deadline passed. You can also request a tax transcript from IRS.gov to verify prior-year filings and confirm what the IRS has on record.

Keep proof of everything. Save e-file confirmations, payment receipts, bank account transfer records, and copies of any IRS notice.

File First, Even If You Cannot Pay in Full

Filing quickly can reduce the harsher late filing consequences. That is often the most important first step after an unfiled return crosses the due date.

E-file is usually the fastest option. If your records are messy, a tax preparer or tax professional may be able to file based on available documents and help you clean up missing details afterward.

Pay What You Can Right Now

Partial payment is better than no payment. Even a modest amount lowers the unpaid taxes that continue to generate penalties and interest.

Common online payment options include Direct Pay, the Electronic Federal Tax Payment System, and EFTPS for scheduled payments. Debit card payments and credit card payments are also accepted, or you can set up a payment plan if full payment is not possible right now.

If you also owe estimated tax payments for the current year, those are separate from any back taxes and carry their own quarterly due dates.

Know Your Options for Penalties, Interest, and Payment Relief

Interest does not stop just because you ask for help. When the IRS approves a payment plan or installment agreement, interest accrual usually continues until the full balance is paid.

That surprises people.

A payment arrangement can prevent the account from falling further behind, but it does not erase the original tax debt. You still owe the tax, and penalties and interest may continue under IRS rules.

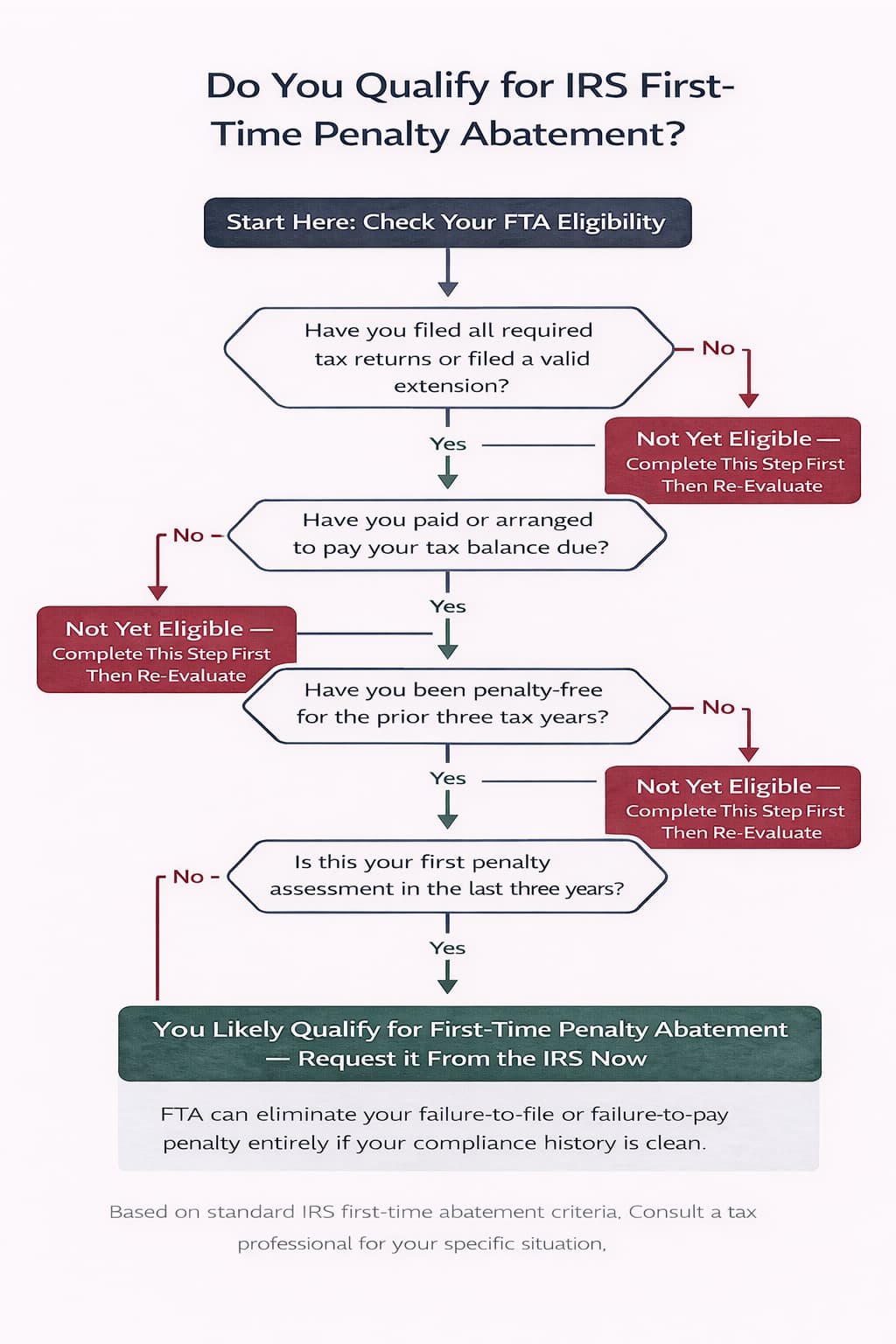

Relief may still be available in some cases. The IRS may consider penalty relief through first-time penalty abatement or through a reasonable cause request, depending on your history and the facts.

Installment Agreements and Other Payment Arrangements

A short-term payment plan generally gives you extra time to pay without a formal long installment structure. A long-term payment plan, often called an installment agreement, spreads payments over a longer period and may involve setup fees.

These arrangements help manage cash flow, but they do not wipe out unpaid taxes. If you owe a large amount, review the terms carefully before agreeing to monthly payments you cannot maintain.

When Penalty Relief May Apply

First-time penalty abatement is a form of penalty abatement for taxpayers with a clean recent compliance history. It may apply when you filed and paid properly in prior years and now have a one-time slip.

Reasonable cause is different. Serious illness, records lost in a fire, disaster relief situations, or other events outside your control may support a request for penalty relief if you can document what happened.

Special Situations That Can Change the Deadline

An extension changes one date, not both. The automatic six-month extension gives extra time to file a federal tax return, but it does not give extra time to pay tax owed.

That point causes a lot of confusion around April 15 and October 15.

If you filed an extension, the return itself is usually due by October 15. Any expected tax balance due was still generally due on Tax Day, so late payment charges may apply even when the return was filed within the extension period.

Some taxpayers get extra time to file under separate rules. Military personnel, overseas taxpayers, people affected by disaster relief announcements, and certain others may receive different deadlines.

Do not assume those rules apply automatically. Check IRS.gov and any official IRS notice before relying on special timing relief.

If You Filed an Extension but Still Missed It

Missing the extended deadline creates a new late filing problem. Once October 15 passes, the IRS can treat the return as late unless another valid exception applies.

Penalties are usually tied to unpaid tax, not just missed paperwork. If little or no tax was owed, the financial damage may be smaller, but the return should still be filed right away.

Military, Disaster, and Other Extra-Time Rules

Military personnel may qualify for postponed deadlines tied to combat zone service or related duty rules. Overseas taxpayers and military personnel serving outside the U.S. may also qualify for automatic deadline extensions without filing a separate form.

Taxpayers in a federally declared disaster area may receive announced disaster relief with extra time to file and sometimes extra time to pay. Eligibility depends on the specific IRS relief announcement, so verify dates and covered locations before assuming your tax return deadline changed.

Avoid Common Mistakes and Plan Your Next Move

Silence makes tax problems worse. When an IRS notice arrives, read it, confirm the tax year involved, and respond by the stated deadline.

Ignoring letters can push an account toward collection activity. That can include stronger IRS action if balances remain unresolved and returns stay unfiled.

Another common mistake is waiting until full payment is available before filing. That approach often increases the failure-to-file penalty while doing nothing to stop interest charges on tax owed.

File the return, pay what you can, review your IRS Online Account, request penalty relief if you qualify, and set reminders for the next tax return deadline. If the situation is larger than one late year, get help early. A tax professional can be especially useful for multiple unfiled return years, large balances, or notices that suggest enforcement risk.

Mistakes That Make a Bad Situation Worse

A guessed balance can create new trouble. Use actual tax records, wage statements, prior returns, and IRS account information instead of rough estimates when preparing a return or choosing a payment amount.

Documentation matters. Save returns, payment confirmations, and correspondence so you can prove what was filed and paid.

A Practical Recovery Checklist

A catch-up plan does not have to be complicated.

File Your Late Return Online With PriorTax

For taxpayers ready to act, filing a late return online through PriorTax takes the same guided steps as filing on time.

Prior year returns are supported, pricing is transparent, and a tax professional reviews every return before submission.

Frequently Asked Questions (FAQ)

What happens if you miss the tax deadline?

File and pay as soon as you can. If you owe tax, the IRS may assess a failure-to-file penalty, a failure-to-pay penalty, and interest. If you are due a refund, a late-filing penalty usually does not apply.

Can I still file my taxes after April 15th?

Yes, you can still file after April 15. Filing late is usually far better than not filing at all because delays can increase penalties and interest when tax is owed.

What if you miss your tax return deadline?

Submit the return immediately and pay what you can. If full payment is not possible, review IRS payment plan options and see whether penalty relief may apply.

What if I missed my income tax return deadline?

You still have options. File now, confirm whether an extension or special relief applied, and respond quickly to any IRS notice tied to that year.

Missing a tax deadline is fixable, but delay makes it more expensive. File first, pay what you can, verify your options with the IRS, and deal with the issue while it is still small enough to control.

Categories: