Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments May 25, 2026

May 25, 2026Missing the tax filing deadline creates one urgent question: can you fix it before the costs get worse?

For anyone asking, “Can I still file my taxes?”, the answer is yes, and the IRS still accepts late returns after April 15.

What changes is not your ability to file, but the financial risk tied to penalties, interest, refund deadlines, and how many years are missing.

Key Takeaways

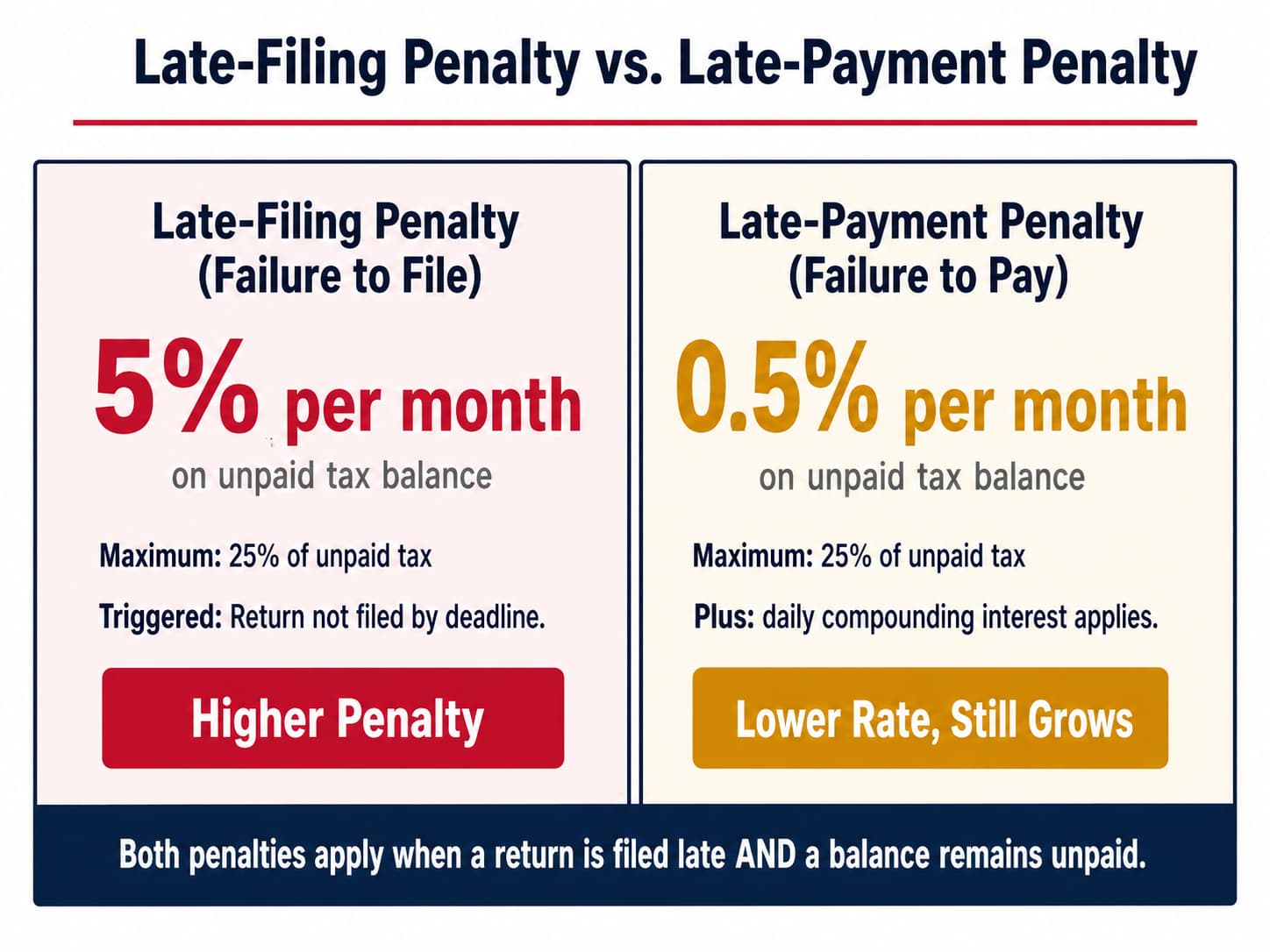

- File the prior-year tax return immediately even without full payment – the late-filing penalty (technically the “Failure to File” penalty) grows faster than the late-payment penalty

- Prioritize earlier refund years first when multiple years are missing, since the 3-year refund rule expires regardless of IRS contact

- Choose e-file when the year is eligible; use paper filing with proof of mailing when older returns require it

- Request an installment agreement after filing if the tax balance due cannot be cleared in one payment

- PriorTax specializes in filing past due tax returns accurately and affordably, with transparent pricing and no hidden fees

Yes, You Can Still File, What “Late” Really Means

The IRS allows filing past due tax returns after April 15, whether you missed one year or several.

“Late” usually means the tax return arrived after the tax filing deadline, and that matters most when a tax balance due exists because the late-filing penalty and interest can start building quickly.

Late filing and late payment are separate problems.

Filing your Form 1040 as soon as possible often cuts the larger late-filing penalty, while paying what you can reduces the late-payment penalty and daily compounding interest even if you cannot clear the full balance.

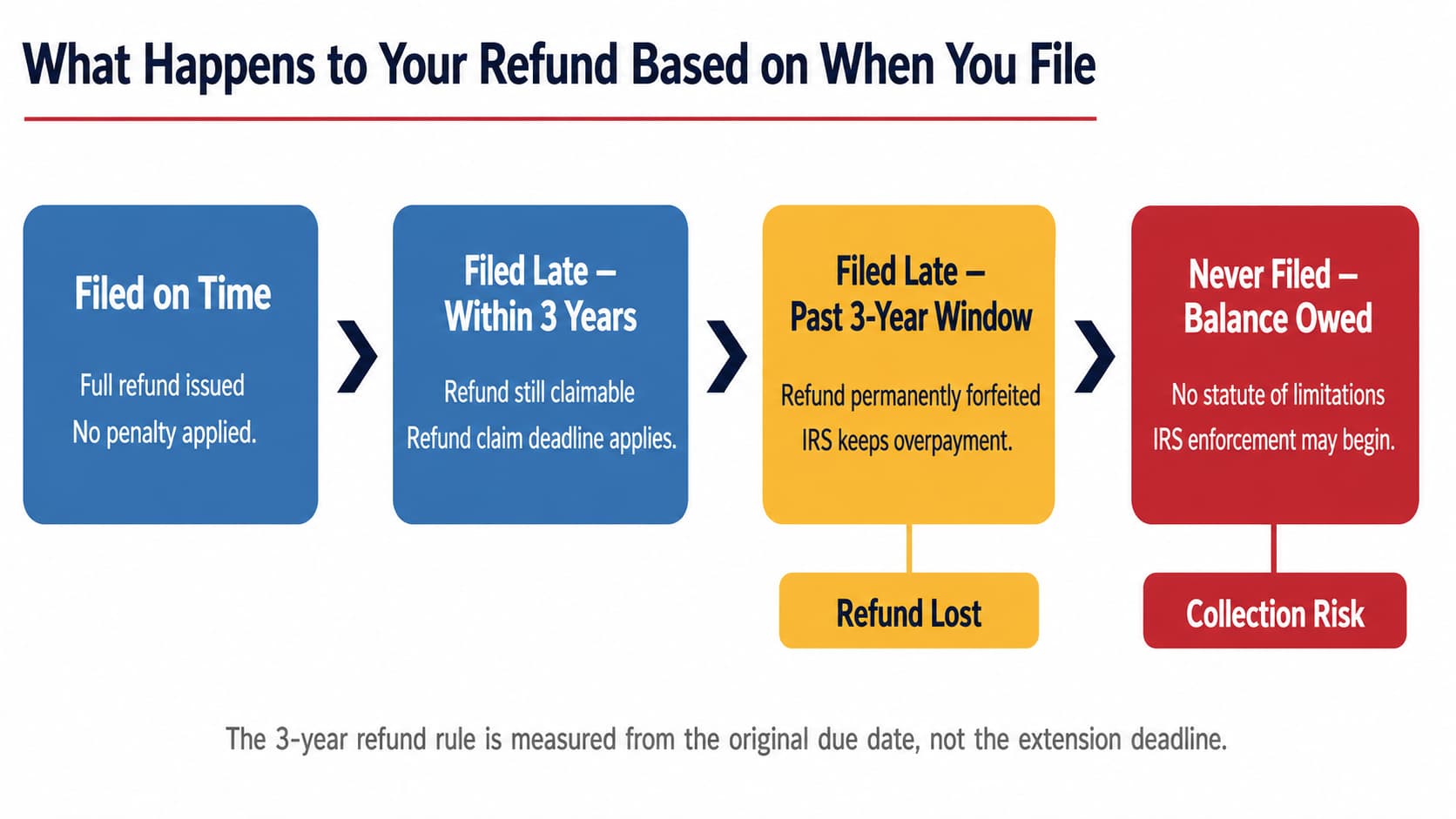

Refund cases work differently.

If withholding, estimated tax payments, or refundable credits exceed your tax bill, you may still receive a refund, but the refund claim deadline can close that window permanently if you wait too long.

State rules add another layer.

A federal return and a state tax return can have different penalties, mailing rules, and e-file availability, so checking your state tax agency matters even when the IRS issue seems straightforward.

Readers who need practical next steps can review how to file late taxes or file back taxes before deadlines tighten further.

Deadlines That Matter: Refund Window, Extensions, and Prior-Year Rules

The most important deadline after April 15 is often the 3-year refund rule.

The IRS generally requires a refund claim deadline within three years of the original due date, which means a taxpayer who overpaid through withholding or estimated tax payments can lose that money simply by waiting too long.

A tax extension helps, but only in a limited way. Form 4868 gives more time to file, not more time to pay, so interest and possible late-payment penalty charges still apply to unpaid tax after the original due date.

A prior-year tax return is still fileable, but the method changes by year. Recent years may be eligible for e-file through approved software or IRS Free File, while older returns often require paper filing and mailing to the correct IRS address for that tax year.

That distinction matters because mailing the wrong year’s return to the wrong place slows processing and can delay both refunds and compliance.

If you missed the tax deadline, speed matters, but using the right year-specific process matters just as much.

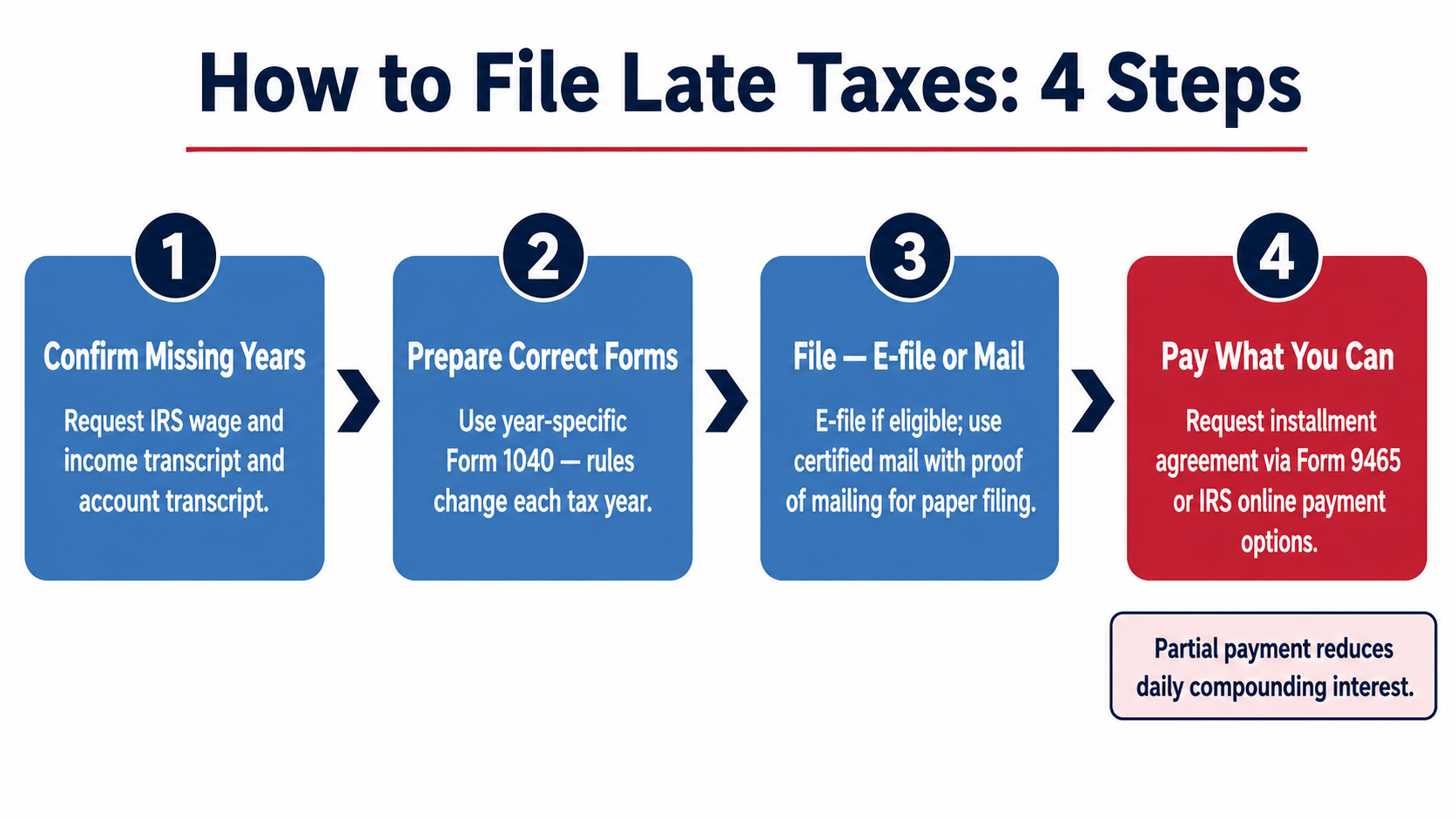

Step-by-Step: How to File Taxes Late (Current Year or Prior Years)

Start by identifying every missing year before preparing anything. IRS transcripts, especially wage and income and account transcripts, show whether returns were filed and what income the IRS already has from W-2, 1099, and other reporting forms.

Each tax year needs its own Form 1040 and tax rules.

Using the wrong year’s forms can misstate tax credits, tax deductions, filing status, and dependents, which creates mismatch notices and often delays processing longer than the original late filing did.

Choose e-file when the year is eligible because it is faster and catches more errors before submission.

Older returns may require paper filing, and proof of mailing becomes important evidence if the IRS later claims it never received the return.

File even if you cannot pay in full. A submitted return stops the late-filing penalty from growing in many cases, and a partial payment made through online payment options starts reducing interest immediately.

Step 1: Confirm Which Years You Need to File

IRS transcripts give you the cleanest starting point. The wage and income transcript shows reported earnings, while the account transcript helps confirm whether the IRS marked a year as filed, assessed, or still missing.

Multiple missing years require triage. Refund years usually deserve first attention because the statute of limitations for claiming that money is short, while compliance years may stretch further if no required return was ever filed.

Step 2: Prepare the Correct Forms for Each Tax Year

Every year stands alone in tax law.

Credits, deduction limits, and line items change, so a 2022 return cannot be prepared accurately on a 2025 Form 1040.

Attach every schedule your income requires. Self-employment income, education items, mortgage interest, and investment activity often need supporting schedules, and leaving them out can turn a valid return into an IRS notice problem.

Step 3: File (E-File If Eligible, Mail If Required)

E-file usually produces faster acceptance and fewer data-entry mistakes. Prior-year e-file availability depends on IRS and software rules, so some older returns must be mailed even when the information is complete.

Paper filing needs discipline. Use the correct address for that year, sign the return, include attachments, and keep certified mail or other delivery proof because mailed returns move slowly through IRS processing centers.

Step 4: Pay What You Can and Set a Plan for the Rest

Partial payment helps more than many taxpayers assume. The IRS calculates interest on the unpaid amount, so every dollar paid now reduces future interest and the late-payment penalty.

An installment agreement can spread the debt over time. Taxpayers often request one online or through Form 9465, and setting a plan early lowers the odds that routine debt becomes enforced collection.

What Happens If You File Late: Penalties, Interest, and IRS Actions

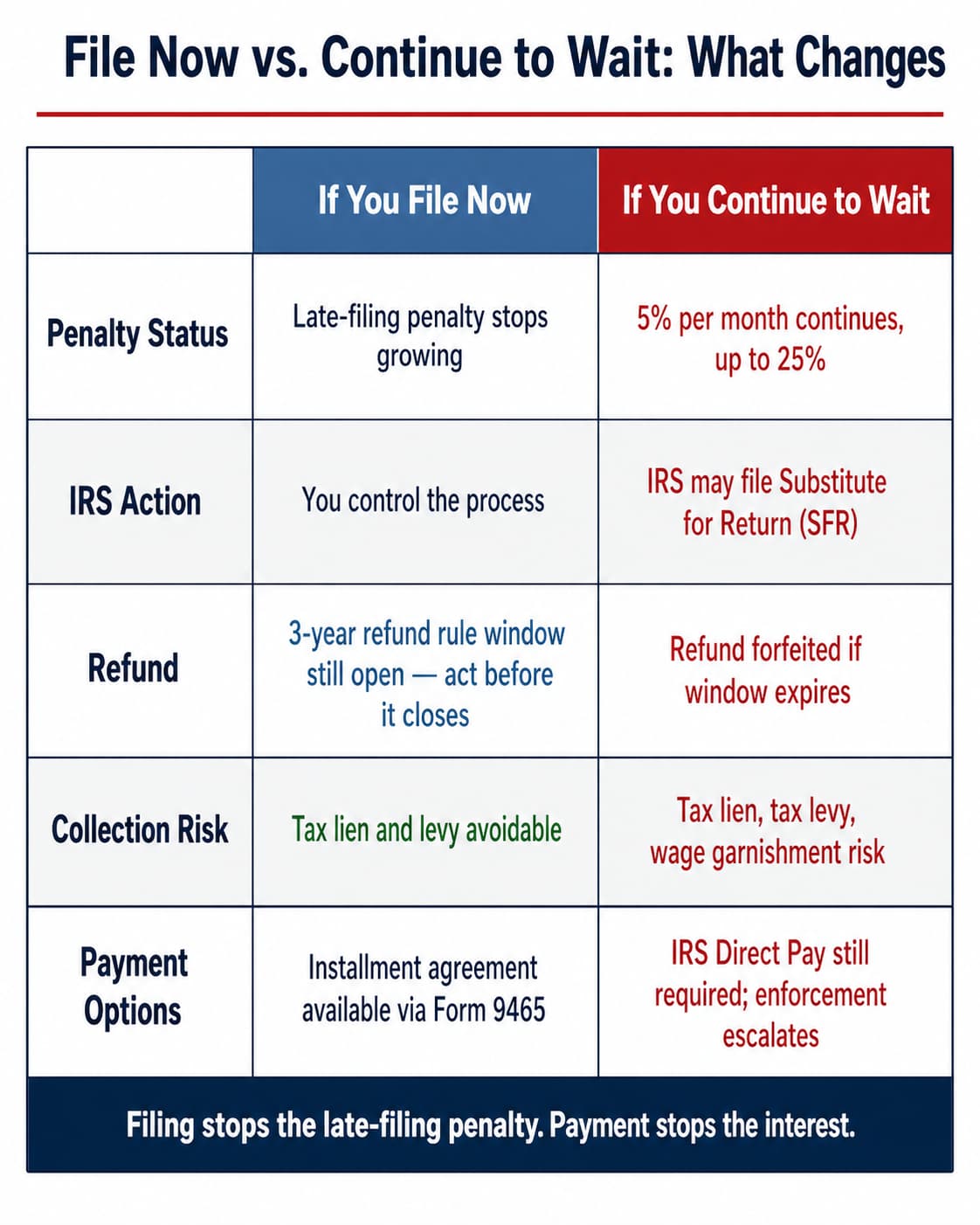

The IRS generally charges a late-filing penalty that is larger than the late-payment penalty, which is why filing first is usually the smartest move when cash is short. Interest also applies to unpaid tax, and the IRS compounds that interest daily, so delay raises the bill even when no new income is involved.

If you are due a refund, late-filing penalties typically do not apply because there is no unpaid tax to penalize.

That does not make waiting harmless, since the refund claim deadline can still erase the refund completely.

Nonfiling can trigger a Substitute for Return, or SFR. An SFR uses income data the IRS already has but usually omits deductions, credits, and favorable filing positions, which often produces a higher assessment than a properly filed original return.

Collection pressure can escalate if notices go unanswered.

The progression may include an IRS notice, then a tax lien or tax levy, and in severe cases wage garnishment, especially when back taxes remain unresolved for years.

How to Reduce the Damage: Practical Ways to Limit Penalties and Maximize Refunds

Fast action changes the math.

Filing immediately can stop the late-filing penalty from increasing, and paying part of the balance through IRS Direct Pay, EFTPS, or card-based online payment options starts shrinking the base on which interest is charged.

Accuracy matters because missed items cut both ways.

Overlooking tax deductions or refundable credits leaves money with the government, while unsupported entries can trigger processing delays or extra IRS scrutiny.

Payment Options If You Owe

IRS Direct Pay works well for many individual taxpayers paying from a bank account. EFTPS is often useful for people who make repeated payments, including estimated tax payments, because it provides a structured payment history.

An installment agreement gives breathing room, but it is not free money.

Penalties and interest may continue until the balance is paid, so larger upfront payments still reduce the long-term cost even after Form 9465 or an online request is approved.

Refund Maximization Checklist (Commonly Missed Items)

Check refundable credits first because they can produce a refund even when no tax is owed.

Earned income-related benefits, education items, and health coverage factors often change from year to year, so assumptions based on one prior return can be costly.

Review filing status, dependents, withholding, and estimated tax payments line by line.

A single wrong Social Security number or omitted withholding figure can turn a refund into a notice, especially on a prior-year tax return prepared from incomplete records.

Examples: What to Do in Common “Late Filing” Situations

A taxpayer who missed April 15 but expects a refund should file quickly and focus on documentation.

Missing W-2 or 1099 forms are not a dead end because IRS transcripts can often reconstruct the income and withholding data needed to claim the money before the 3-year refund rule expires.

Someone who owes taxes but cannot pay in full should still file now, pay what is possible, and request an installment agreement. That sequence usually costs less than waiting, because the late-filing penalty can outpace the late-payment penalty.

Multi-year nonfilers need a plan, not guesswork.

The IRS often looks for six years of returns for compliance, but if a required return was never filed, the statute of limitations generally does not begin, which gives old nonfiling issues a long shelf life.

Common Mistakes to Avoid When Filing Late

Waiting until you can pay everything is the most expensive mistake.

Filing and payment are separate duties, and treating them as one decision often turns a manageable tax balance due into a larger debt.

Wrong-year forms create avoidable trouble.

A prior-year tax return prepared on the wrong Form 1040 can miscalculate tax, omit schedules, and cause the IRS to reject or manually rework the filing.

State returns get missed all the time.

A taxpayer may fix the federal side and still face state penalties because state tax return deadlines, refund rules, and filing systems differ from IRS procedures.

Documentation and Accuracy Pitfalls

Estimated numbers can backfire when the IRS already has exact figures from employers and payers.

Using IRS transcripts instead of memory lowers the chance of mismatches that lead to notices and delayed refunds.

Simple clerical errors still matter. Missing signatures, bad SSNs, and math mistakes slow paper filing in particular because manual correction takes longer than electronic validation.

Key Takeaways and Next Steps

You can still file, and the right move is usually to act now rather than wait for a better moment.

Filing past due tax returns protects refunds, limits penalties, and gives you more control before the IRS chooses the next step for you.

Start by confirming missing years with IRS transcripts, then prioritize years with likely refunds and any years already tied to an IRS notice or SFR.

Choose e-file when available, use paper filing carefully when required, and pay what you can even if the full balance is out of reach.

When to Get Professional Help

Professional help makes sense when several years are missing, an SFR has been filed, or self-employment and multiple 1099 forms make the return harder to reconstruct. A careful review can also uncover credits and deductions that reduce back taxes or increase a refund.

Common Questions (FAQs)

What happens if I don’t file by April 15th?

You can still file after April 15. If you owe taxes, the IRS may charge a late-filing penalty, a late-payment penalty, and interest, so filing quickly usually lowers the total cost.

Is it too late for me to file my taxes?

Usually, no. Most taxpayers can still file late, but anyone due a refund should watch the refund claim deadline because the IRS generally will not issue that refund after the three-year window closes.

Is it possible to still file taxes?

Yes. You can file a current-year return late and also submit prior-year returns, though older years may require paper filing instead of e-file.

What happens if you are late filing your taxes?

If you owe, penalties and daily compounding interest can grow until you file and pay. If you are due a refund, penalties typically do not apply, but you still must file to claim it.

Categories: